In his book, the neuroscientist Dr Daniel J. Levitan indicates why our time remaining to invest may pass by faster as we age than when we were younger. He explains “that our perception of time is…based on the amount of time we’ve already lived.” The Organized Mind, (Penguin Canada Books, Toronto, 2014)

Time from a financial perspective

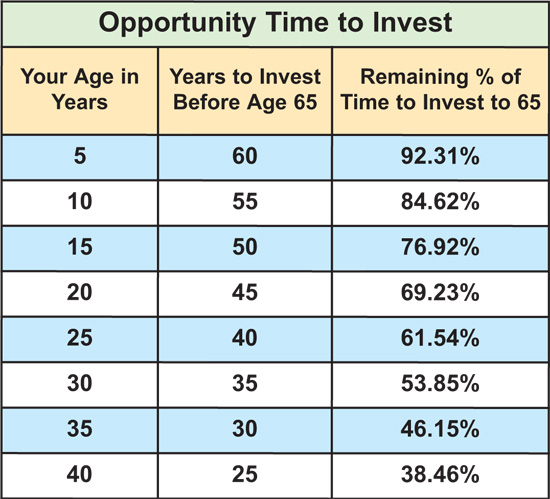

Dr Levitan’s observation may apply mainly to the anxiety people experience as they age. As the time to retirement shortens, some may begin to fear that they might not have saved enough for retirement. Procrastination takes its toll on compounding investment gain potential. When looking at an average retirement age of 65, the two tables in this article reveal the profound truth about the dwindling of time and the shrinking opportunity time remaining to invest as we age year by year.

Graph Source: Adviceon©

Time offers the opportunity to create wealth.

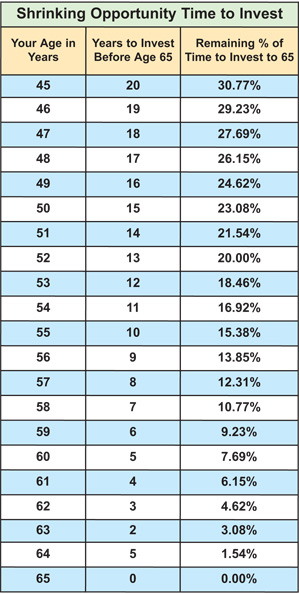

We must sincerely acknowledge the fantastic opportunity investment time provides the investor. Most people have had lots of time within which to invest. At age 35, we cross over the halfway mark of the time remaining to invest our hard-earned income to the age of 65; at age 45, approximately only one-third of our time is left! Please look at the shrinking opportunity of time in the second table, which shows how the availability to have compound gains working for you drastically decreases as time passes.

Some parents begin wisely investing for their children right after birth and get time to work on their side early.

Graph Source: Adviceon©

Why does investment opportunity time get lost?

Greed and fear work against investing. Many people get caught up in timing the market when influenced by either of the two emotions, greed or fear. Here’s why this never works. First, desire compels people to buy when the stock market (and potentially a fund unit value) is higher. Conversely, fear causes many to sell when the stock market’s value (and possibly a fund’s unit value) is lower.

When you can’t seem to begin investing, make regular investments in promising companies to benefit from a method referred to as dollar-cost averaging (DCA) to level out the peaks and valleys of the market by purchasing at regular intervals. If the value of shares in a fund decreases, you buy more units. Conversely, if they go up, you buy less. Time spent invested in the market, not timing the markets, counts.

Don’t just look at an investment fund’s most recent performance. Instead, look for long-term investment performance over one, three, five and ten-year periods. Moreover, make investment decisions with the help of a professional advisor who has access to investment managers.