We face a rapidly ageing population.

Since the 1920s, the ratio of seniors over 85 has more than doubled. This number increases into the 2050s for those over age 85.

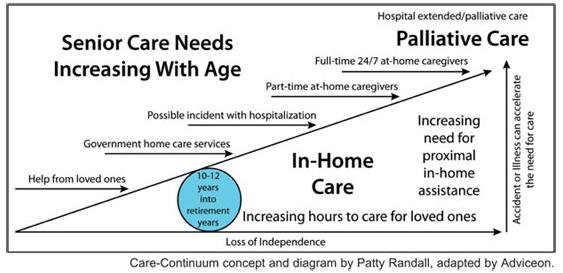

Who will care for you in your old age? When our health is fine, it is hard to imagine that we may, as many will, lose the ability to manage basic daily activities such as bathing, toileting, walking, dressing, feeding, or moving from bed to chair. Many also lose mental faculties that we often take for granted, such as memory, logical or conceptual thinking or referencing dialogue with others. Without assistance, it is near-impossible to function without these capacities.

Long-term Care Insurance (LTCI) is an insurance contract with an insurer designed to provide care for chronic illness, disability, or accident, which are more likely to occur as we age.

Some families are incapable of caring for a senior. LTCI protects our families from the financial strain of providing long-term care, just as important as life and disability insurance, which protects the income of younger families. The question is, who will financially support long-term care for you? LTCI is not just for seniors but for those who become similarly incapacitated at any age.

Without a plan, your choices may be limited. Planning for our long-term care independently is essential because our government healthcare budgets and initiatives are limited. They generally place people in government-funded facilities that have beds available. As we witnessed during the pandemic, many long-term care facilities had difficulty coping with the virus’s spread.

Most people overlook the enormous expense of paying for a private long-term care facility (some cost up to a quarter of a million dollars for five years). Why are they so expensive? They offer 24/7 high-level nursing care in a highly secure environment. Note: Anyone can call a few private long-term care companies and inquire about their care costs.

Ageing baby boomers who are retiring will increasingly depend on long-term care insurance, either paid for by themselves, their children, or professional health care services.

The need for Long-Term Care Insurance is increasing as medical interventions and medications keep us living longer.

- Every year, about 50,000 strokes occur in Canada. A stroke is the leading cause of a transfer from a hospital to a long-term care facility.

- Nearly 10% (1 in 11) of Canadians over age 65 are affected by Alzheimer’s disease or related dementia.

- An increasing demographic (7%) of Canadians age 65 and over are residing in healthcare institutions.

- An additional 28% of Canadians age 65 and over receive care for a long-term health problem outside a healthcare institution.

As the populace ages, more care for the elderly, such as respite care (additional home care services), will increasingly be needed to provide family members with the medical guidance and support they need to continue caring for their loved ones. With this in mind, are our families financially prepared to deal with peripheral costs associated with providing long-term care for loved ones?

- A study by Dr Marcus Hollander and Neena Chappell of the University of Victoria found that approximately $25 billion worth of unpaid care is provided willingly by family members and friends in place of paid care.

What does Long-term Care Insurance (LTC) offer? Long-term care insurance provides money for the care you desire and need. With LTC insurance, you have:

- Broader choices about the quality and amount of care you receive.

- An increase of options when determining where you receive care and by whom.

Sources: Statistics Canada, pre-baby boomer info, Canadian Institute for Health Information, Alzheimer Society website, Statistics Canada