Let’s compare taxed and tax-free investment returns to see this advantage. First, let’s look at investing outside of your registered retirement savings plan (RRSP). If you have a marginal tax rate of 40% and invest $2,000 per year for the next 30 years at an average 7% annual return, you will accumulate $120,864.

Now consider if you invested the same money in the RRSP. If you contribute $2,000 every year to your RRSP for the next 30 years, and you earn an average 7% return, you will earn $202,146. The tax-advantaged growth empowers your RRSP as the growth is compounded over a long period of time.

Why is it important to save for retirement? RRSPs can give you the financial resources you need for a comfortable retirement that will meet your lifestyle requirements. Many Canadians are living for 30 years during retirement with a need to provide an income.

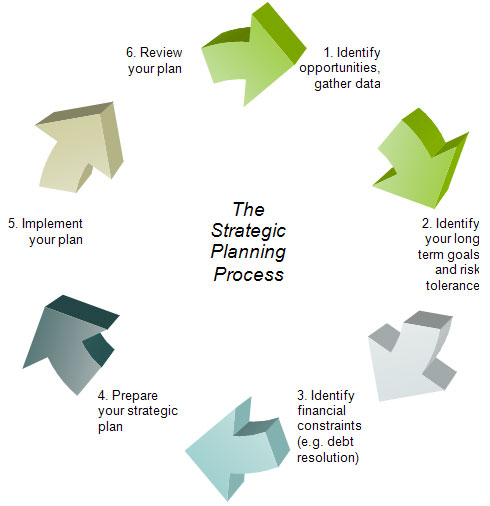

Investing is the strategic planning process, not the final goal It is important to realize that investing is not the goal. The goal is based on a future result that you aim for using mathematical calculations. Investing is what you do in the meantime while facing a multitude of circumstances in the world that affects the market where stocks and securities lose or gain potential to grow, which means, intermittently affecting your control of the end results in relation to your goal.

While you are young and have a family and/or close dependents, you also want to enjoy life and create memories. You want to live in the present to minimize fear of the future during the investment process, being mindful that preparing to retire means engaging in the process with an advisor using timeless principles.

Perhaps you’ve decided that you must accelerate your combined RRSP savings if you are to possibly realize your retirement dreams. Here is a strategic process that works all year round, well ahead of, and therefore, eliminating the annual RRSP deadline frenzy. This investment also works well when investing using TFSAs.

A systematic investment strategy called Dollar-Cost-Averaging (DCA). By pre-arranging a schedule of making equal monthly investment purchases of a mutual fund, you can realize big advantages:

1) Get your RRSP money working earlier. Every year, a good deal of money begins working long before the RRSP deadline. This gets part of your fund money invested earlier every year in small amounts you can afford. DCA allows for a convenient pre-payment of your annual RRSP contribution, instead of in the last anxious moments of February before the annual deadline.

2) You can profit from more gains after buying during market downturns. You needn’t worry about market-timing decisions when you buy your mutual fund units. Investing a fixed dollar amount every month adds a benefit over the year. You will purchase more mutual fund units when the price is lower, fewer when the price is higher. While consistently purchasing throughout market declines, when units cost less, you buy more units with the same dollar. Thus, fears of the market dropping in value are replaced with the knowledge that you will eventually own far more fund units over time, as long as you continue to invest in the same scheduled manner when the market is down. The purchases are scheduled, not “timed”. There is a vast difference.

Not even the experts know exactly when the market will peak, or stop declining. This means that by waiting to purchase at a lower unit price, an investor might miss buying lower if the market begins climbing back suddenly. But, if you schedule consistent buying, using DCA, you won’t miss buying the lower-priced units.

What is the upside of DCA in a lower priced market? Fund units purchased during temporary market downturns can be very profitable once the market recoups any loss. Subsequent upward moving markets will greatly increase the value of every unit held (especially with the addition of those lower-priced bargain units bought when the market value declined, and as it inclines above each unit price purchase during periods of market gains). More units bought at lower prices, both while a market loses value and while the market swings back gaining momentum during a major bull market growth spell, offer the potential for future profit.

3) One more benefit. You’ll be less influenced by market fear factors if you remember: Investing is a strategic process, not the final goal. Dollar-cost-averaging fund purchasers are isolated from negative market psychology. Contrary to the crowd, they now automatically buy through periods of opportunity when the price is low, the time when most people often do the opposite — sell out of fear. Dollar-cost-averaging encourages determined, intelligent, and disciplined investment behaviour.

Do your heirs expect to inherit an old homestead property, a family cottage, a residence, your farm, an art collection, furniture, or business shares? They may have to be liquidated by the estate, perhaps at a loss, to pay any existing tax liability. Life insurance proceeds may help to side-step probate, or estate administration tax, and can cover any estate liabilities that could impinge on bequests that you want to make.

Make sure that your gifts stay in your family. Deemed dispositions of capital assets at death occur even if an asset is willed directly to an heir. A capital gains tax liability remains in the deceased’s final tax return and reduces the value of the estate.

5 Methods to reduce taxes that will be due upon your death.

Use the spousal (and disabled child) rollover provisions of RRSPs or RRIFs.

Leave assets that have accrued capital gains to your spouse to defer tax.

Leave assets without capital gains to other (non-spouse) family members.

While you are alive, gradually sell assets having capital gains, to avoid dealing with the capital gains all at once in your estate.

Purchase life insurance to cover capital gains taxation in the estate.

Taxes may be payable on gains.

Income-producing real estate, a second residence, or cottage, and any other assets left to surviving family members, such as shares of a business, of stocks and investment funds may face capital gains taxation.

You may also want to consider charitable donations to lessen taxes in the estate. Hire an estate planning lawyer and make sure your Will is updated and includes your estate planning directives.

TFSAs can help transfer money to your heirs.

Money accumulated in a TFSA does not attract taxes at the time of death. If you want to create increased transferable after-tax wealth, consider moving money into TFSAs from non-registered investment accounts. Note: It is important to get an Advisor’s guidance, and perhaps an accountant to implement this in a careful tax plan.

Be careful, though to also consider taxable implications when considering selling non-registered assets. Ask your tax advisor if you will be triggering a taxable gain? Possibly utilize TFSAs to their maximum potential and monitor the comparative tax impact of transferring wealth from RRSPs/RRIFs to heirs of the estate.

We endeavour to deliver unparalleled service in group retirement and savings plans.

Canadian Defined Benefit Contribution plans and Group RRSPs have continued to play a growing role in Canada’s retirement landscape. We can help employers streamline and improve their retirement benefits for employees.

Pensions in Canadian Retirement

Statistics Canada recently released some good information on retirement savings trends in our country. For families in which the major income recipient was aged 55 to 64, 8 in 10 held either RRSPs or employer pension plans (EPPs). It is noteworthy that at each age level, median pension holdings were substantially higher, at $244,800, than those who only hold RRSPs.

A company that has a pension plan or assists employees to achieve their retirement is an employer of choice, particularly among high-quality seasoned and experienced employees.

We will work with you to develop the Group Retirement & Savings Plan best suited to your organisation’s needs.

Life insurance has been called the foundational strategy of building and protecting your net worth. The initial stages of your financial strategy should include adequate life insurance coverage.

The following 7 tips will give you a template for your life insurance planning for a lifetime.

Term life insurance is affordable protection when you are young When young, term insurance coverage offers the lowest cost per thousand dollars of coverage. It comes in various renewable periods of time, for example, 5-,10-, 20-year term and term to age 100.

Upon each renewal of term insurance, the cost can increase and may have a final term period ending at a certain age such as age 65, 75 or age 100.

Many term plans can be converted to lifetime insurance coverage without medical evidence, that will continue to cover you for the duration of your life.

Life insurance can pay off large accumulations of debt Many owe thousands of dollars on their credit cards or a large amount of business debt.

Replace the debt monkey with cash money Term life insurance often solves debt concerns. It can offer you the peace of mind that you will not be saddling your family with ongoing debt.

If you own a business You and your partners can enter agreements to redeem debt or buy business interests providing cash to your heirs.

Debt-free succession plans work better Infusions of cash into a business can help a succession plan to work well.

Your life insurance plan can change to adapt to your needs Review your life insurance during each of life’s stages. Our circumstances change dramatically and so do our needs for life insurance. It may be time to review your life insurance and verify beneficiaries, policy amounts and any riders associated with the plans. As you evolve financially, so do your life insurance needs.

You can protect your family when you have young children When you are newly married and starting a family, life insurance is purchased to provide tax-free capital in case one of the parents should die.

When your children are going to college protect your liabilities Many of us tap into our savings to help meet their children’s tuition and housing expenses. We may purchase a child’s first car, or pay him/her an income for one or more years. If you die without providing continuing support, your young adult child may need to quit seeking a higher education due to a shortage of funds to pay for tuition and expenses.

Special Estate Planning solutions When your estate will face a large tax bill, or you desire to leave a large sum of money to an heir or a charity, there are life insurance solutions.The proceeds of a death benefit can solve estate-related problems such as paying an estate’s tax liability on capital gains.

As you approach retirement, you may have accumulated assets that will be taxed as capital gains: such as a cottage, business, equity fund holdings, or a stock portfolio. Life insurance that continues for a lifetime, such as Term to age 100 or Whole Life (or Permanent Life)—can help pay the income tax due in your estate.

This can also replace an estate’s money used for paying taxes on remaining Registered Retirement Savings Plan (RRSP) or Registered Retirement Income Fund (RRIF) holdings, as these funds are fully taxable to the estate where there is no surviving spouse or dependent child.

It can also pay off large business debts that may be left as an ongoing liability, weighing on a surviving spouse’s financial security.

You may have an heir who will need a large sum of capital invested to provide a lifetime income from a trust fund. This is often the case with disabled children who may have special needs which can be expensive over a lifetime.

You may want to leave a significant sum of money to a charity of your choice.

You may want to transfer large sums of wealth in a controlled manner using life insurance beneficiary directives which may in some cases circumvent probate and notification to others when you desire privacy in your estate outside of your will.

Your exact life insurance needs can be calculated Life insurance specialists use a calculating system referred to as “capital needs analysis”. Consider insuring the adults in your family. The breadwinner’s income can be replaced to protect your family’s financial security. You may have debts that you’d like redeemed. Final expenses can be paid. A mortgage can be paid off. Retirement money can be generated. There are many good reasons to strengthen your financial security with life insurance.

It is necessary to calculate the capital needed over any short or long period to meet any financial situation. Call for an appointment to have us review your life insurance.

Note: Talk to your advisor about potential tax exemption changes to investment components of life insurance.

Did you know that you cannot pass on your Registered Retirement Savings Plan (RRSP) or Registered Retirement Income Fund (RRIF) holdings tax-free to your heirs? Once the second spouse dies, all monies in an RRSP or RRIF are taxable as income in your final tax return unless there are dependent children.

An eligible individual is a child or grandchild of a deceased annuitant under an RRSP or RRIF, or of a deceased member of a Registered Pension Plan (RPP) or a Specified Pension Plan (SPP) or Pooled Registered Pension Plan (PRPP), who was financially dependent on the deceased for support, at the time of the deceased’s death, because of an impairment in physical or mental functions. The eligible individual must also be the beneficiary under the Register Disability Savings Plan (RDSP), into which the eligible proceeds will be paid. 1

In most cases, significant tax may be due, depending on your marginal tax rate and final calculations in your estate. Consider talking to your advisor about buying a joint last-to-die life insurance policy timed to pay after you and your spouse die. It can equate to a small percentage of your RRSP/RRIF holdings per year to make up for the taxes due on what has become, for some, a small fortune.

When planning your estate. It is important to consider how taxation will affect the future distribution of your estate. For individuals who are married, when the first spouse passes away, the assets are generally able to be rolled over tax-free to the surviving spouse. However, when the last surviving spouse passes away, all assets are deemed to have been sold at the time of passing, and this includes your Registered Retirement Savings Plan (RRSP) or Registered Retirement Income Fund (RRIF) holdings.

Concerns about leaving wealth to the next generation. Registered assets are taken into income in the year of the surviving spouse’s death, and taxes must be paid. These taxes will be due after the death of the second spouse, where there are no dependent children. An eligible individual is a child or grandchild of a deceased annuitant under an RRSP or RRIF, or of a deceased member of a Registered Pension Plan (RPP) or a Specified Pension Plan (SPP) or Pooled Registered Pension Plan (PRPP), who was financially dependent on the deceased for support, at the time of the deceased’s death, because of an impairment in physical or mental functions. The eligible individual must also be the beneficiary under the Registered Disability Savings Plan (RDSP), into which the eligible proceeds will be paid. 1

Without an eligible dependent, a $500,000 RRSP or RRIF could be reduced to about half the sum after the death of the second spouse (assuming the highest tax rate). How can this be avoided? How can you leave more of your wealth to the next generations?

A joint last-to-die life insurance policy may be a solution. A joint last-to-die policy insures two lives, usually two spouses, for the purpose of paying for an estate’s tax liabilities, such as capital gains on a cottage or business. In most cases where there also exists significant family wealth in RRSPs or RRIFs, taxes will eventually be due upon the second spouse’s death. At that time, the entire remaining RRSP or RRIF funds are brought into income. Though this is not creating a liability as such, the taxation of large holdings of registered monies can deplete a family’s overall wealth.

By purchasing a joint last-to-die life insurance policy, the taxation of assets in a family’s estate plan can be offset by the significant life insurance proceeds.2 In the above example, a joint last-to-die life insurance policy for $250,000 would replace the estate value lost to taxation, therefore helping to preserve the estate’s net worth more fully for the family. This is especially true if the RRSP or RRIF owner expects to leave the entire amount to their heirs.

What about the life insurance premiums? The premium for the life insurance policy to pay for the estate’s tax loss through RRSP or RRIF final estate taxation is usually a small percentage of a significant registered investment portfolio compared to the much larger tax bite. The death benefit may be partially tax-free. 2 A joint last-to-die policy can also be structured to reimburse all premiums paid into the policy, thereby minimizing the cost to the estate for a strategy designed to save money.

When RRSP assets are present in an estate, there are a few steps to follow to assist transferal in the event of inheritance, death or separation.

A surviving spouse can transfer the full amount of a spouse’s RRSP as a refund of premium by rolling it into his or her RRSP or RRIF, life annuity or term annuity depending on age. Preferably, name your spouse as the beneficiary under all RRSP plans when you set them up, or make this provision in your will. Note: Your advisor will be able to look at your situation and advise you.

If you leave no surviving spouse but there is an adult child or grandchild who is ‘financially dependent’ upon the deceased at the time of death, the full RRSP can be transferred tax-free to the child’s RRSP or used to buy an annuity or RRIF. Minors, however, must use the funds to purchase an annuity with payments to age 18. Note: Your advisor should be consulted to determine if an individual is ‘financially dependent’.

In most cases outside of financial dependency, the funds are taxed in the hands of the deceased on his or her last tax return. Life insurance strategies can offset the large tax liabilities associated with RRSP/RRIF assets that seniors will face, thus increasing inheritances.