It is critical to take responsibility and save for retirement

In the information age we are inundated with data, to such a degree, we can get distracted from our principal wealth creation goals. Neuroscientist, Dr. Daniel J. Levitin points out in his book, The Organized Mind, with regard to a never-ending stream of social media, news, and career info, that “our brains are hungrily soaking all this in because that is what they’re designed to do, but at the same time, all this stuff is competing for neuro attentional resources with the things we need to know to live our lives”. And one of the key things we need to know is how to get our finances on track for retirement!

Why people fail to plan A recent article in CNN noted after surveying 1,000 people about retirement that “many people spend more time researching which car to buy or where to go on vacation than they spend on their investments — more than half said they had spent five hours or more doing research the last time they bought a car, and 39% said they spent more than five hours exploring vacation possibilities. Meanwhile, a mere 11% said they had spent that amount of time evaluating investment options”. Levitin makes a case for the need for categorical thinking if we are to wade through the information best suited for our lifestyle. Applying his wisdom, the secret is to determine how you break down your financial strategies categorically speaking, and then determine how you prioritize your processes in relation to your goals. By asking how you organize your finances it forces you to look at and list the most pertinent categories with a realistic application for financial survival:

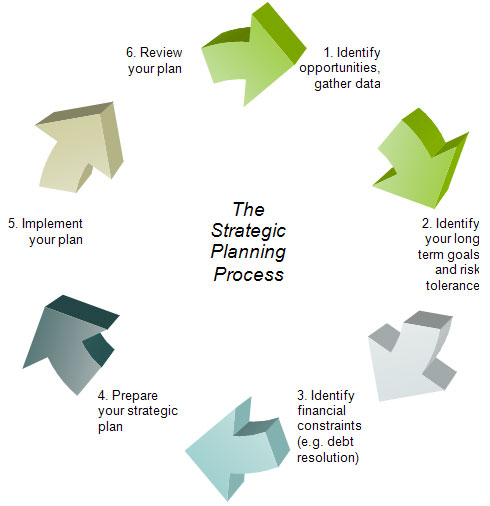

Organize categories as retirement priorities.

There are many factors to consider in the cycle of ongoing, systematic strategic financial organization as you can see in the diagram above. However it is vitally important to apply your powers of concentration to organize strategy in the following key categories, areas within which financial advisors are trained to assist you:

- Net worth Add up all your assets and subtract your liabilities to get your financial net worth.

- Retirement income resources Within your assets of your net worth, determine the specific amount earmarked as saved for retirement from which to draw an income for a lifetime. Bear in mind that some of your assets will be fixed (not liquid for cash) such as your residence.

- Weigh debt interest against investment interest Debt accumulation must be mastered as it will drain any good retirement plan.

- Expiration potential of income resources Based on how long you might live – your life expectancy – calculate just how much cash the funds can deliver for your lifetime per month. Then based on how much you determine you will realistically need to cover expenses per month, calculate when the money would run out or if you have enough saved to last a lifetime. Add in pension income sources. Income resource planning needs to accommodate reasonably achievable long term goals while considering your risk tolerance.

- Investment action plan You must have a systematic method of investing in order to beat the ravages of time and inflation.

- Invest with a mind to save tax Utilize all the tax planning strategies available with the government’s registered accounts.

- Invest for wealth creation If you have five or more years left you must invest if you haven’t reached your necessary accumulation from which to draw an income. Seek investment advice from a professional advisor.

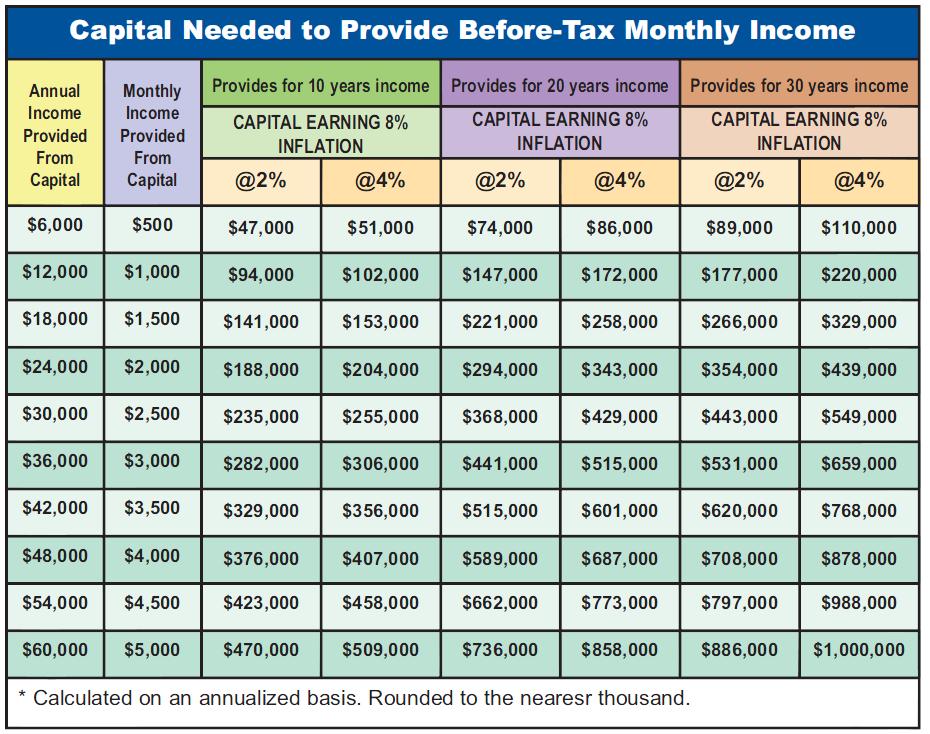

- Invest for wealth preservation Once you have accumulated your nest egg, develop strategies to protect against losing capital, yet remain invested in suitable vehicles for your age. The following graph will denote how much money is necessary for a prolonged period of time in retirement.

- Get good investment counsel Here is the need to use a financial advisor who daily works in the realm of financial calculations while looking at your future income needs. An advisor will review your plans and investment performance periodically to help keep you on track.

Successful people delegate, so can you

Dr. Levitin points out that “successful people – or people who can afford it – employ layers of people whose job it is to narrow the attentional filter. That is, corporate heads, political leaders, spoiled movie stars, and others whose time and attention are especially valuable have a staff of people around them who are effectively extensions of their own brains, replicating the functions of the prefrontal cortex’s attentional filter”.

In the same way, in order to be successful at retirement planning you may need to engage the help of a professional advisor, someone who often does not charge for his or her services (some advisors are paid via other means), as well as fund specialists and/or investment managers trained to help you achieve financial success.

An advisor can help organize and govern your finances

Again, the logic of The Organized Mind, when applied to finance is simply to get financial guidance – applying the resources of fiscal counsel available. Levitin summarizes this concept of getting someone to handle the daily distractions of life – and unfortunately many view financial organization as a distraction lumped in with all the other media distractions, when it comes down to getting through a basic day, month, or year! Little wonder most people procrastinate when it comes to their finances.

These highly successful persons–let’s call them HSP–have many of the daily distractions of life handled for them, allowing them to devote all of their attention to whatever is immediately before them. Daniel J. Levitan Ph. D. – The Organized Mind -published by Allen Lane

We all want to be successful in our career and workplace as well as in our investment planning. Why not talk to your financial advisor about implementing an organized financial plan – bearing some of the burden to help you get on track – after you study the graph below depicting the capital needed on which to retire. And ask yourself, “is it time that I get help?”

Graph Source: Adviceon