Banks follow established rules, which include asking a business owner to collateralize a loan, not just with business assets but also with personally owned assets, such as a principal residence and cottage. Collateralization can require collateralising a spouse’s co-owned assets, even if the business is incorporated.

Add to that a possible collateralization of any assets of a partner or adult child (and their spouses) who also share in ownership. Small business owners can lose their shirts if they default on a loan.

What if an owner dies? It is unwise to assume that a good relationship with the bank will continue if the heir of a small business or a partner is not in favour with the bank manager. Bank managers can change or apply strict policies while reassessing the leniency shown to previous owners or administrators.

Eliminate doubt in a family business, such as a farm, by insuring the oldest owners and succeeding generations using joint-first-to-die policies or individual life insurance policies. In the case of a non-family business, each owner/partner should be insured to cover the company’s debt. When the life insured dies, the tax-free life insurance proceeds can be used to pay back loans, win back ownership, and discharge any personal assets liens.

What if there is a critical illness? For the same reason, small business owners should consider purchasing a critical illness (CI) insurance policy for each principal business owner and key persons. CI insurance could pay off a considerable bank debt if one were to experience a significant illness such as a heart attack or stroke. One could become incapacitated and need to be bought out by a partner or an heir (there should be a buy-sell agreement in place). The risk of a loan being called increases when an owner-manager is sick, and the bank manager loses confidence in the debt-paying influence of that owner.

After the death of an individual, every estate must file a final (or ‘terminal’) tax return. All assets are deemed to disposed of at the time of passing, and this can trigger probate fees and other expenses.

A certificate of appointment (“Probate”) or Estate Administration Tax (EAT) is not always necessary to actualize the transfer of certain assets. Much depends on how the asset is held during one’s lifetime, and the value of the asset transferred. Some institutions will not require probate for assets under a certain amount. Concerning jointly-owned real property, and bank or investment accounts, these assets will pass to the surviving joint tenant by right of survivorship. In cases where joint ownership of assets is considered for estate planning purposes, it would be prudent to obtain legal advice.

Life Insurers offer life insurance policies, segregated funds, and term funds, which may designate one or more primary beneficiaries, and further contingent (secondary) beneficiaries, allowing probate/EAT to be circumvented entirely, enabling direct access to those funds without joint ownership or survivorship of a joint tenant. Segregated funds and term funds are classified as deferred annuity policies, and as such, these assets can help lessen the overall fees charged on your estate. Monies pass privately and directly to your beneficiaries, outside of your estate and the probate process.

Concerns for Estate Planning

In Ontario, Probate fees were the forerunner of the new Estate Administration Tax (EAT), which is to shift to the Minister of Revenue. An Executor/Trustee will now have to file a detailed summary of assets that are distributable under the will. The Ministry reserves the right to take up to 4 years to assess, or the right to reassess, making the Executor/Trustees responsible for that reassessment. Executors and beneficiaries may face liabilities if estate assets distribute before assessment or reassessment. How does an Executor reclaim assets already distributed?

Assessment powers are not minor With the introduction of the estate administration tax (EAT), the government has given the Minister of Revenue audit and verification powers patterned after the federal Income Tax Act, thus giving the Minister of Revenue the right to assess an estate in respect of its EAT liability.

Estate trustees may be personally liable for the claims of creditors that cannot be paid as a result of an improper estate distribution. It will be an offence for an estate trustee to fail to make the required filing with the Minister of Revenue or where anyone makes, or assists in making, a false or misleading or omitted fact in connection with the estate trustee’s filing. Because offences are punishable by fine, imprisonment or by both, errors and omission insurance may be needed by executors handling larger estates.

Potential Legal Issues for Estate Trustees and Executors

Imagine if you are a personally chosen friend of a deceased person with $1.5 million in assets, who previously selected you as Executor/Trustee of his or her estate. Though duty-bound, you may feel that the risk is now very high if an error occurs. Consequently, you may want to off-load the potential liability to a professional accountant and lawyer to present all the documentation for EAT.

Consider that the costs of such a transfer of liability could rise to the maximum of 6% per professional (two professionals would mean 2 x 6%) of the value of the Estate. This could bring the total cost of dealing with EAT to a maximum of 13.5% of the estate value. In the above case, fees could cost upwards of $202,500.

Segregated and Term funds may offer investors an edge over other investment products in the province of Ontario when it comes to planning someone’s Estate. Segregated and Term funds also offer estate privacy of the distribution of money under the insurance act.

Note: Not applicable in Québec as notarial wills do not need to be probated by the court and, for holograph wills and wills made in the presence of witnesses, probate fees are minimal.

In business and investment, more significant gains are associated with both business success and variable risk. Six risk factors are examined below, along with constructive ways to deal with them.

Risk increases with the potential for gaining wealth in the markets

There is no such thing as gaining wealth without risk. Risk generally increases within any business or investment when the potential for gain is greater. Mutual funds diversly invest in the stocks of many companies. If a business succeeds, its stock price (and dividends) can increase in value and pass that worth on to the fund unitholders.

If many companies’ stocks increase in value in a mutual fund, the investor’s wealth can increase relative to the resulting total net increase in all of the fund unit’s value. In the short term, a mutual fund, like any business, can fluctuate in value, so the risk of losing money in the stock market increases if equity fund investments are held for only a short period.

Defining Investment Risk

The potential for gain generally increases the longer you hold equity fund investments. Because economic performance is uncertain, an investor who seeks growth by investing in the ownership of companies via equity mutual funds cannot have zero risk. Most successful investors realize that the following risks exist yet invest despite these:

• Interest rate risk when increasing could negate gains of certain income funds investing in bonds.

Solution: Maintain a balanced portfolio including equity funds and different types of income funds: money market, short-term bond, and long-term bond funds.

• Business failure risk could deplete the value of any one company’s stock.

Solution: Consider investing in equity mutual funds because they hold many different stocks.

• Purchasing power risk is an alarming reality faced by everyone due to inflation’s historical average, which has been between 3% and 4%.

Solution: Calculate inflation into your retirement planning and consider investing in equity mutual funds over the long term, with the potential to build sufficient wealth to meet increased future budget demands due to inflation.

• Market risk occurs because markets are cyclic, rising, correcting, and occasionally declining.

Solution: Diversify your funds, investing in a family of domestic mutual funds and internationally among foreign mutual funds as not all markets move together.

• Opportunity risk occurs when you cannot invest your money for a potentially better return, such as when you are invested in a locked-in type of investment, such as term deposits, or have tied up your income in monthly payments.

Solution: Try not to lock up all of your money, keeping some in money market funds over any given period.

• Liquidity risk occurs when you cannot quickly sell a given investment, such as an extensive real estate portfolio.

Solution: Invest in mutual funds. If money is urgently needed, funds can be sold and money accessed on any business day with possible costs.

Here are some tips to help you lighten the load of Elder-Care:

• Plan your caregiving carefully. Don’t be ashamed to ask for and get help from your siblings or others when caring for a family elder—let others share the load—tell them how they can help, and let them know you expect it! They can clean, cook, take them to the doctor, shopping, or church, and take them to their home for a little break/holiday, etc. • Be honest about what you can truly handle. Be honest about your time when you are home and what you can realistically achieve. Don’t let your housework stay undone due to your over-commitment to the elder. That isn’t fair to you or your family. • Assess government and public resources. Find out what services are free or available as paid-for services—learn what your community offers in senior care. • Prioritize your to-dos. In this way, you’ll know what needs immediate attention, such as their physical comfort and safety. Determine if any problems, such as a lack of heat or air-conditioning, water leaks, or mould accumulation in the elder’s environment, needs attention. Delegate help to family members or friends concerning their skill set, career, or financial ability to help. • Assign care tasks to the elder that they can do. List the jobs to define what they can and can’t do. Involve the elder as far as possible in the plan, if they can cook their meals and bathe themselves, and let them know this is henceforth expected of them. • Outsource where needed. Discuss who you might hire with the elder, and where applicable, expect their input in the decision. Maybe you must bring in a house-cleaner weekly and hire a handyperson. • Let the elder assist you financially. You may be putting them up in a space in your home, and they might use your resources, so it is not out of line to ask them to help pay your bills (perhaps via rent). The elder is now retired, so they ought to reach into their investment income (if they have wisely invested or have gained other assets) or pension income to share in the expenses and perhaps buy and prepare their food. • Decide to make informed decisions. Don’t procrastinate to make the necessary changes and improvements because years of frustration may accrue as “things unattended only to get worse”. • Meet with a lawyer and financial advisor. If the relative increasingly depends on you to help in their estate planning, employ a good lawyer they can trust; write an up-to-date living and testamentary will. • Review to determine if there may be life insurance needs for the funeral and burial expenses ahead of time. If there is, consider buying a policy and have siblings or heirs split the premium. • Assess any tax and debt liabilities. Assess retirement savings, investment holdings, other assets and all liabilities to create a mini net worth snapshot to determine the potential net need for life insurance. Then select the amount necessary. Check if any cash values can make current cash income while maintaining an old policy the elder may own. Determine who will be the Power of Attorney (PA). • Become an advocate. Don’t be afraid to take the elder’s side. Many are not used to today’s current culture and need kind understanding. So speak up for their rights and causes; never bully them or ignore their cries for help or justice as they face our healthcare system, unfair medicinal prescription fees, or rude gestures from others. Dialogue with physicians (and get second opinions) when necessary for their well-being. • Maintain a happy attitude. If you keep your good humour and remain positive, you’ll lessen the stress factor. Caring for elders can tip your emotional scales, so laugh a little, even at yourself! • Review and respect their historic life’s excellent and fun aspects with you. One day your elder won’t be around to show your appreciation and love for their positive role in your life. Tell respectful stories about their hero or heroine qualities. They probably did rescue you by overseeing your younger days while feeding and clothing you. Don’t put them down for failures—forgive them. They may have “been there” for you, so recall the best days of their life to realise they were needed, appreciated, and loved for who they are. • Maybe write a book on their story. Why not review their life story in a journalised small book of their history—to leave a legacy to your family to show appreciation and take your mind off the stressful negatives? It may reveal redemptive qualities; to teach your younger generation by example—to impress the younger generation by the elder’s influence, such as perhaps: their character developed by war, or persistence during poverty, or a corrective life-change, their hard work that led to business success, or a healed relationship via forgiveness, or their involvement in charitable giving, or their volunteer work to help others, etc. • Stay ahead of burnout. Get some rest and exercise weekly to protect your mental and physical health. Fulfil all your responsibilities, and maintain all your meaningful relationships. Be sure to get the R&R you need to stay graceful, strong and vigorous as your elder ages and becomes more dependent on you. • Find unanimity in an elder-care support group. They can share their ideas and help you make decisions, help you not to feel alone, and help you face stresses and problems as they relate their wisdom obtained by experience. Getting ideas and compassion from other caregivers caring about you doesn’t hurt.

Caring for an older adult is not a job that comes with training or gets a lot of thanks—it is something you take on, usually out of love. It can be an unappreciated Herculean effort—but at least you’ll know you did your best at the end of the day. Your love is what counts.

Every so often, you can take a self-inventory and restate your primary purpose in caring for an elder. This will help you overcome the temptation to complain, throw in the towel, or send the elder to a rest home too early.

You may want to consider Longterm Care Insurance for yourself or your loved ones, which helps pay for services the family members may not be able to provide. Talk to your advisor about the life insurance policies available for these services.

Here are ways to protect your successor financially.

Allow the potential successor to get involved in managing important team projects. Try to increase the successor’s financial insights and general responsibilities over time. Allow independence while ensuring that the right professionals assist the successor, such as a good accountant and insurance agent.

Consider visiting other family businesses that have transferred their business through continuity planning.

Establish mentors and advisors for the successor. Consider setting up a board of directors if one is not in place. Implement leadership training programs.

We do not suddenly become what we do not cooperate in becoming.— William J. Bennett

Protect your assets during Succession in the following ways:

Cover your key persons. Use life and disability insurance to cover the cost of replacing an owner, successor, contingent successor, or a key executive in the event of death or disability.

Ensure debt redemption. Life insurance proceeds can pay off bank loans and other liabilities—paid at the owner’s death. Also, consider critical illness insurance, which would pay up to $2,000,000 if the proprietor were to become critically ill.

Provide income replacement insurance. Disability insurance benefits can provide income to an owner, successor, or key executive if disabled over specific periods. The payment paid as a benefit to a disabled insured, places less payroll burden on the company.

Fund a buy-sell agreement. Life and disability insurance proceeds can fund a buy-out upon death or disability, where two or more owners are in business (effective for current or succeeding generations).

Fund a stock redemption. When other members of the family own stock, you can buy life insurance for the owner and make the successor the beneficiary. This will provide cash upon the owner’s death to allow the successor to buy the stock of, say, sisters or brothers, based on a pre-determined formula related to equalizing the estate.

Fund capital gains tax liabilities. If significant capital gains will impair the company, reduce personal assets, or disallow a legacy of a cottage or other asset, use a permanent life insurance product designed to pay off all capital gains liabilities.

Create capital to equalize your estate. In the future event where one child will inherit the company, life insurance can be purchased by the owner or spouse to pay the non-involved children a tax-free cash benefit in predetermined amounts, clear of probate. To avoid resentment, you can inform these children that they will be treated fairly in the overall estate.

Let him, who would move the whole world, first move. — Socrates

Maintain relationships during succession

Keep your banker informed. What would your banker do if something happened to your firm’s current owner? Who else knows of the company’s loans or actual financial status? Introduce your successor (and the succession plan) to your banker and review all the company liabilities. Reveal your life insurance planning to the banker that can offset liabilities in the balance sheet.

Sustain client relationships. Introduce your successor early on to your key clients. Perhaps host client appreciation events.

Harmonize the successor with the constituency. The key players will help the company survive, including critical suppliers, influential families within and without; shareholders you hope will seek minimal dividends instead of future growth; employees, especially those holding company stock; and the key executives.

Diversify sources of retirement income. Keep your retirement investments separate from your business. Consider purchasing segregated funds, separating your assets from the company while reducing exposure to creditors. Avoid investing your profits into the business without developing your independent retirement resources. Thus, you will not need to rely on the company to create an ongoing retirement income, though you may receive dividends and income from the business.

Move towards financial independence of your business. Though you leave a legacy to your successor(s), you can ensure that the inheritance will have sufficient funds to survive during and after the succession. Drawing from your retirement savings can reduce dependency on business income (or dividends).

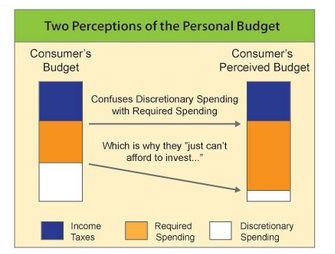

After most people have paid for their necessities, there seems to be little left over for investing.

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?

If you see yourself as a “consumer”, you may experience that there is never enough paycheck left at the end of the month for investing. However, is this caused by a lack of income or your own spending patterns? The first barrier to investing is a “perceived lack” of investment capital, often not reflecting reality. Unfortunately, what we think often becomes our reality.

Investors have personal discipline Conversely, “Investors” take an honest mathematical look at their expenses, separating discretionary income from what one needs to live on, knowing that impulsive buying decisions, even to purchase many small things on sale can add up.

This disciplined viewpoint allows them to have money to invest. Once paid, the first “consumption” decision can be to purchase an investment suitable to their goals and objectives. The rest of their paycheck is then spent with no worries on required consumption for the rest of the month.

Investors get good advice, and then act. Many people are impatient or confused when it comes to the science of investing. True “Investors” all have a key characteristic that makes for success — taking the right action with professional advisory assistance. They also understand that without experience and knowledge, investments decisions can be made in haste, and potentially destroy an otherwise good investment plan.

Condominium living has become an option for homeowners who want to reduce the many responsibilities of a single-family residence. Most condominium corporations assume these tasks and are a popular choice for young and middle-aged purchasers who are too busy or prefer to limit their day-to-day home duties such as garbage and snow removal, home maintenance and repairs. Condominiums are also attractive to retirees who want to own without any strenuous activities that consume time or who want freedom and security to travel without worrying about pre-retirement duties.

A purchaser needs to obtain an up-to-date status certificate for the unit and have it reviewed by a real estate lawyer. Real estate agents generally make a condo purchase and sale agreement conditional upon a satisfactory review of the Status Certificate. Under the Condominium Act, a condominium corporation has ten days within which to produce a status certificate for anyone who requests one (upon payment of the prescribed fee, which is currently $100). The Act also establishes what information a status certificate must contain.

What is a status certificate?

A status certificate provides a snapshot of everything that may concern prospective purchasers, including its overall financial situation and budget relative to the amount of money in its reserve fund (a savings account maintained for significant repairs and replacements of the common elements such as a new elevator or chiller); the rules by which unit owners are expected to abide; and whether the condominium corporation knows any circumstances that may increase to the standard monthly expenses.

It is important to determine if a condominium corporation is involved or expected to be involved in litigation, and an up-to-date status certificate may reveal that the unit is subject to a “special assessment,” which is a sum of money the condominium corporation believes must be collected from the unit owners to cover an unforeseen expense. This knowledge of a special assessment may affect what a purchaser is willing to pay for a unit.

Your mortgage provider may also want to let you know that your lawyer has reviewed the status certificate as a requirement of the sale.

Here are five wealth creation principles that will remain true forever.

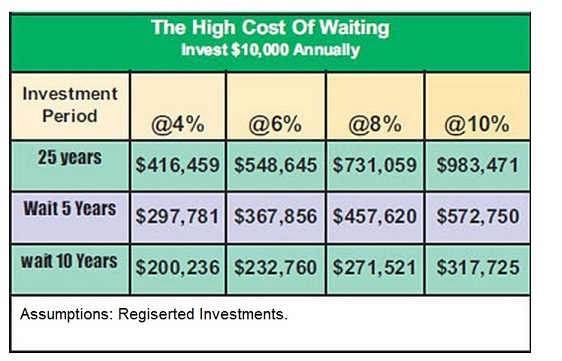

1. You must get time on your side by investing early in your lifetime. Time adds value to money. Delayed investing shortens your time, which increasingly requires the compensation of higher and higher returns to meet your retirement goals. Examine the following graph to see how time affects your investment growth.

Source: Financium

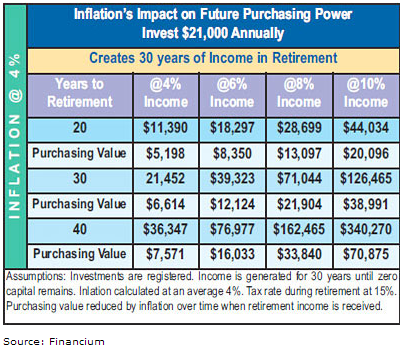

2. Your investment growth must exceed inflation. If you earn 8% on a $10,000 investment per year, over 20 years with inflation at an average 4% your actual investment will grow to $457,620, but your actual buying power in the future will only be $208,852 (while your money is growing, inflation is increasing the cost of goods). The graph below indicates how inflation might affect your investment’s future buying power.

3. Algebraic factors apply to investing. You can indicate your multiple on capital invested by applying mathematical rules, factoring in both time and rate of return.

· Double Your Money: Rule of 72. To find out how many years it will take to double your money, divide 72 by your average annual rate of return.

· Triple Your Money: Rule of 113. Divide 113 by your average annual rate of return to see how many years it will take to triple your invested money.

4. Taxation can reduce your investment returns.

Every dollar of tax retained through tax-planning is a dollar earned.

· Deduct what you can against your income. Business owners have the advantage of deducting many operating expenses from their revenues.

· Contribute to registered investments. For both business owners and employees, registered investments may allow deductions against earned income and may offer tax-deferral.

· Defer as much taxation as possible. The beauty of registered investments is that they allow some tax planning benefits depending on your income, and capital available to invest.

5. Become an active investor. It is important to begin investing early in life when you get your first job or begin your career. By beginning early, you can have the above stated mathematical laws of doubling and tripling your money working for you. Many wait far too long before investing and lose the value that time can add to a good investment portfolio by increasing the future accumulation of investment money.

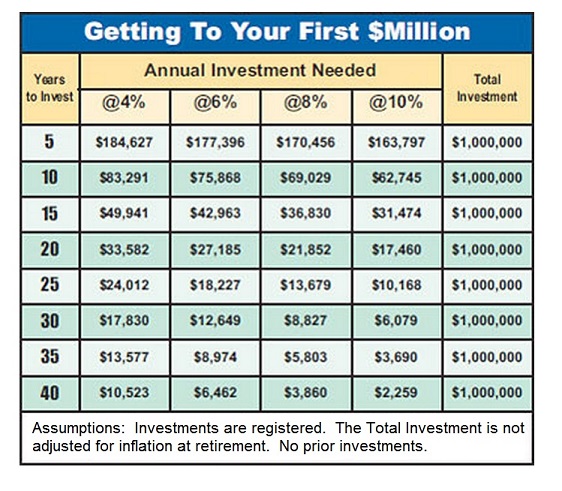

The following table will let you know just how much you will need to invest to accumulate one million dollars.

If you were to have a stroke, heart attack, or severe operation—a disability to which you could not take care of your affairs, who would take over? What if this was the last day you could make a mindful decision on your behalf?

You transfer directorial powers over your affairs to a Power of Attorney

In such a situation, a Power of Attorney (POA) allows people you trust to manage the prescribed affairs of your life.

Without a POA, your family though ready to pay your bills, and help manage your bank account and your investments, for example, may need special court approval to act for you. They could face a bureaucratic nightmare to acquire authority to pay your bills (from your provincial public trustee).

• Clarity can be defined. A POA leaves no room for misunderstanding the range of authority over your assets. You may need to set restrictive clauses in a POA that addresses your unique concerns.

• You will give up the powers of your signature The POA relinquishes the control of your signature and all the authority associated with it. Unless it states otherwise, the attorney may use a POA immediately upon signing.

• It must be witnessed. Improper witnessing annuls legal completion and sets the POA up for contention. Thus make sure the document is witnessed correctly.

• Be careful of restrictions you may not want to be included. Some broad-form POAs include optional clauses often left included, whereas they may not be applicable. These may have regulations on the attorney you may not want to impose.

• You may want to restrict beneficiary changes. If you want the attorney to have power over changes of beneficiaries to life insurance or investment assets, make that clear. If not, clearly restrict the right to change beneficiaries.

A warning which may or may not apply to you

Unfortunately, once authorised with your directive powers, an attorney could feel it is their privilege to become an “empowered benefactor” of your (you, the donor’s) estate once they lose capacity. So, having a lawyer articulate your specific wishes in your Power of Attorney documentation is a good idea.

To empower and entrust another with your authority, may be the last time you can make a responsible decision on your behalf, so make it carefully.

Where significant wealth is involved, consider a POA explicitly designed to give powers to assist in governing your financial affairs.

A proper estate plan will include an updated Will and a plan to avoid paying too much tax on investment assets such as stocks, bonds, mutual funds, and other properties that may have accrued capital gains. It will seek to minimise probate, pay off debts and prepare to meet specific family income needs. Estate planning often includes detailed life insurance planning designed to pay out a benefit upon the death of one whose estate is about to wind down.

When transferring your assets, including mutual funds, using a Will (also referred to as a Testamentary Trust), the key is to position as much of your wealth as possible to pass to your heirs. If you hold equity mutual funds that buy and hold stocks, they may have accrued capital gains. There will be a deemed disposition of all your property at fair market value at your death. For some, this could mean that there may be an existing capital gains tax liability. There are a few things to assess as you begin an estate plan.

Assess your tax liability. List each separate asset you own, the purchase price and date, and its current value. Include your non-registered investments in stocks, bonds, and mutual funds. Have your accountant assess what the tax liability will be.

Assess how you and your spouse can defer taxes Property willed to your spouse can be rolled over tax-free on your death. Your spouse will inherit the assets at the property’s entire adjusted cost base (cost amount). The taxation of the investment will then occur when your spouse disposes of the property or at the spouse’s death. This tax deferral is beneficial, especially if you have significant holdings in equity mutual funds invested for value as in large-cap or blue-chip stocks. Alternatively, you can choose to transfer any asset to your spouse at fair market value on death and recognise the accrued gain or loss.

Assess RRSPs if you have dependent children RRSPs can be transferred tax-deferred to your dependent children or grandchildren, even if a spouse survives you.

Assess income splitting using a testamentary trust By establishing a testamentary trust in your will, you will be able to maintain control during your lifetime over the use of your assets such as a mutual fund investment portfolio. The trust can provide guidelines for the treatment of these assets after your death. The trust document can specify the split of income among heirs. Carefully planned income splitting may allow for significant tax savings.

Assess insurance solutions There are estate planning solutions that only insurance can offer, providing both personal and business solutions to ensure you have financial security. First, assess your tax liabilities with an estate lawyer and/or accountant and make estate plans to determine how to pay them. Consider the following various insurance plans, such as life insurance where the capital gains tax liabilities are substantial.

Personal insurance solutions to protect you and your family include:

• Life Insurance

• Critical Illness Insurance (CI)

• Long Term Care Insurance (LTC)

• Estate Preservation

• Individual Health and Dental plans

If you own a business, insurance solutions include:

• Partnership Insurance

• Buy/Sell Agreements

• Key Person Insurance

• Business Disability Insurance

• Business Office Overhead

• Collateral Loan Insurance

• Group Health Benefits

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?