Amortisation refers to the number of years it will take to repay your mortgage in full. Based on your down payment and current legislation, amortisation periods can run up to 30 years.

Shorter amortisation periods allow you to accelerate paying off your mortgage. The other advantage is that you will pay less interest the more the timeline shortens. The tradeoff is that you will pay more for your monthly payment.

The mortgage payment and method need to unify with your overall financial plan. For example, a mortgage of $400,000 at an average fixed rate of 5% and a 30-year amortisation will have a $2,134 monthly payment, and you will pay $368,506 interest over the 30 years. Reducing the period to 25 years, you’ll pay more at $2,326, but your total interest expense will be reduced to $297,924, saving $70,882.

In our calculator section on this website, we have mortgage calculators, which may prove helpful for planning.

Canada Mortgage and Housing Corporation (CMHC) provides Homeowner Mortgage Loan Insurance, which is required by law to insure lenders against default on high-ratio mortgages.

A high-ratio mortgage This a mortgage with a loan value of more than 80% of the value of the home purchase price (the borrow puts down under 20%).

Note: Bear in mind, legislation may change from the date of this article. Talk to your mortgage agent for an update.

A conventional mortgage This is a mortgage with more than a 20% down payment, which means it has less than 80% of a loan to value ratio — less than an 80% stake in the home’s equity value when purchased.

Homeowner Mortgage Loan Insurance required by law

When a person is buying a home, a new homeowner, in most cases, takes out a mortgage. A mortgage is a loan taken out by a borrower referred to as the mortgagor from a lending institution, referred to as the mortgagee. The property is used as security for the debt. Homeowner Mortgage Loan Insurance is required by law to insure lenders against default on a high-ratio mortgage.

You repay the principal amount loaned to you The principal is the actual loan amount that the mortgagor is expected to repay to the mortgagee (loaning institution). Additionally, the interest is paid over the repayment period (amortization) of the mortgage.

A mortgage is a fully secured loan A mortgage is a fully secured form of financing. Thus, the interest you pay is usually less than with most other types of financing, such as when you buy a car or use a credit card. Once you have built up equity value in your home, a mortgage can finance many different things, including:

Constructing a new home

Purchasing an existing home

Consolidation of debts

Financing a renovation

Financing the purchase of other investments

Financing the purchase of investment property

How do you qualify for Homeowner Mortgage Loan Insurance?

The home is in Canada.

For CMHC-insured mortgage loans, the maximum purchase price or improved property value must be below $1,000,000. Note: Legislation may have or change at any time.

Consideration to How Much Can You Afford

Before you begin shopping for a home, it’s essential to know how much you can afford to spend on homeownership. You will want to plan ahead for the various expenses related to homeownership. In addition to purchasing the home, other significant expenses include heating, property taxes, home maintenance, and renovation as required. Two simple rules can help you figure out how much you can realistically pay for a home. You must understand these rules to understand if you will be able to get a mortgage.

Ask your mortgage agent what the typical minimum down payment is currently for the purchase price of the dwelling, depending on the dwelling type.

Single-family and two-unit dwellings

Three- or four-unit dwellings

Typically, the minimum down payment comes from personally owned resources. However, a down payment gift from an immediate relative is acceptable for dwellings of 1 to 4 units. For eligible borrowers, additional sources of down payment, such as lender incentives and borrowed funds, are also permitted. Check with your lender for qualifying criteria and availability.

Your total monthly housing costs, including Principal, Interest, property Taxes, Heating (PITH), the annual site lease in the case of leasehold tenure and 50% of applicable condominium fees, shouldn’t represent more than 32% of your gross household income (Gross Debt Service (GDS) ratio). Use the GDS form to calculate how much you can afford in housing costs to be eligible.

Your total debt load shouldn’t be more than 40% of your gross household income. The Total Debt Service (TDS) ratio is your PITH + the annual site lease in the case of leasehold tenure and 50% of condominium fees (if applicable) + payments on all other debt / gross annual household income. Add up your costs and determine your Total Debt Service ratio using the TDS form.

It would be best also to consider closing costs (for example, legal and land transfer fees) equivalent to 1.5% to 4% of the purchase price. Many first-time buyers are surprised by these costs.

Closing costs include but are not limited to one-time items such as lawyer fees, GST and PST as applicable, land transfer tax if applicable, adjustments, etc., to allow you to complete the house purchase.

Other requirements may apply and are subject to change.

Definitions: Since the buyer/borrower is pledging the property, he/she is “mortgaging” the property and is known as the “mortgagor”. The lender is the recipient of the pledge and therefore is the “mortgagee”. The mortgagor mortgages the property to the mortgagee.

Many people prefer not to risk not knowing if their mortgage rate will climb higher due to rising interest rates. Many on a fixed budget want to reside in their home peacefully, not worrying about the potential for increasing rates. We all have to understand our risk tolerance on the one hand and our desire for practical frugality on the other.

When the bank rate rises .25%, variable rates can climb higher. Variables are flexible in the financial market. As such, the market affects most variable mortgages by a significantly higher extrapolated percentage of increase (factors which are applied differ among banks). For this reason in an economic environment of rising interest rates, it may be in your best interest to review and possibly reform variable mortgages or interest-only mortgages to a more guaranteed period of five years or higher.

Do the math, asking yourself if you are sure you want to proceed at a fixed rate.

The upside is that with a five-year term, you can know your expense precisely for the entire period. Conversely, the upside of the added risk of the variable rate is that you may not see an increase (as we do now in several banks) and you might even see a fluctuating decrease of rate.

Give me a call, or contact me via my website to discuss your options.

As a dedicated mortgage professional, I can access numerous lending institutions offering unique mortgage products. First-time homebuyers or those either with a mortgage for renewal or looking to refinance, give us a call. You needn’t look any further as we offer great options as a one-stop broker.

Not all products are the same. Our goal is to reveal the options available for you in Canada, to offer superior mortgage products with reasonable terms and rates. The good news is that we don’t tether to any single lender giving me the freedom to help you find mortgage success without biased advice. Not only that – we will work hard with you to ascertain decisions for your future.

Feel free to ask me any questions you may have regarding mortgages, and I will promptly guide you to a fitting solution. Reach out to me – I am a licensed professional ready to advise.

We have been blessed with low interest rates affecting lower mortgage rates. Have you thought about what happens to mortgage rates and how a household’s expenses go up when these rates rise?

Some mortgage thoughts to ponder:

Variable mortgages. Variable-rate mortgages can be a good option when facing declining rates in the short term. And they can be risky if rates rise. Ask your mortgage advisor what mortgage plan suits your needs?

When it’s time to renew your mortgage. Consider that you have a chance to work with an independent mortgage expert to save money. Watch for the letter that tells you it is time to renew or your notices coming in from your financial institution.

Pay your bills and credit cards on time. Even phone company bills not paid can end up on your Equifax report. When applying for a new mortgage, your lender can see your credit score just when you need to appear in good standing as a responsible borrower.

Don’t apply for credit everywhere. Avoid signing up for store credit cards because such applications trigger a credit inquiry. Too many inquiries make it look like you may be strapped for cash flow.

Mortgage HELOC debt versus total debt. High-interest debt can be rolled into your mortgage if the interest rate is lower than your other loans. Plus, you may be able to include renovation costs in your new mortgage. Just be careful not to increase your HELOC (home equity line of credit) ratio close to your home’s value. There is always a temptation to use up your equity. Note: Talk to your mortgage advisor about the pros and cons of raising HELOC debt tied to your home if home values decrease dramatically or when bankruptcy occurs.

Know your mortgage prepayment penalty. To get out of your mortgage early, the right mortgage with a lower penalty could save you a lot of money! Compare these penalties when shopping for your new mortgage with your mortgage expert.

View mortgage pay-downs as an investment. A pay-down will pay it forward into your net worth. Thus prepayment privileges are essential! If you make monthly payments, consider paying your mortgage weekly or biweekly to reduce the amortization period.

Give your mortgage an annual checkup. Keep your mortgage healthy – give it a yearly checkup. Even a minor tweak can better position your real estate planning.

Diversification advantage Mutual funds offer the investor the benefit of maximum diversification, with minimal exposure to any one stock. You pool your investment with the combined capital of other investors, which allows everyone to invest in many companies, not just focus on two or three larger stocks.

Fund managers usually diversify among at least 20 companies, investing no more than 10% of the fund’s total dollars into any one security.

Other advantages of mutual funds

• You can buy additional units of a mutual fund at any time.

• An automatic purchase plan called dollar-cost averaging (DCA) lets you invest equal amounts at regularly scheduled intervals. You buy more fund units when the prices are lower, fewer when prices are higher, thus averaging out the price of the units purchased.

• Mutual funds can be registered in RRSPs or RRIFs.

• Dividends, where applicable, are easily reinvested.

• Some fund companies allow transfers between their funds without charge.

Employee Retirement Plans incorporate the following:

• Analysis of available investment vehicles and associated yields

• Investment tracking and reinvestment alternatives

• Individual financial and investment planning

• Establishment and management of individual registered and non-registered retirement savings plans such as self-directed RRSPs, group RRSPs, & RESPs with the following: investment funds, segregated funds, and labour-sponsored funds.

Group Retirement Options

When your employees retire or are approaching retirement, they will need help through this period of change. Professionals are available to educate your employees about all available retirement income vehicles. We offer the expertise and services to ease the transition to retirement for your retirees:

• Retirement income projections

• Establishment of retirement income vehicles such as RRSPs, RRIFs, LIRAs, LIFs, annuities

Individual Group Investment Products

Whether you are making investment contributions to save for future expenses or retirement, the Group Investment Program allows you to take control of your personal portfolio and achieve your financial goals with peace of mind.

• Lower investment management fees

• No front- or back-end sales charges

• No deferred sales charges

• No minimum investment

• Self-directed RRSPs

• No annual administration fees

• Consolidated statements

A Registered Education Savings Plan (RESP) is a savings plan registered with the government that can help you save for your child’s post-secondary education.

Money invested in an RESP grows tax-deferred. The government helps contribute to your savings with education grants.

Later in life, as your child enrols at a qualifying post-secondary institution, you can withdraw the funds for educational purposes. The payments made from these funds are called Educational Assistance Payments (EAPs).

Invested income and government grants received when withdrawn from the RESP are taxable. You do not pay tax on the contributions you made using your own money. Then these amounts are taxed in the tax return of the student – usually with little or no tax payable as students generally will be in the lowest tax bracket.

How do RESPs help my money accumulate?

Starting to use an RESP for your child early, while they are young, gives you more time for your contributed funds to grow.

The Canada Education Savings Grant (CESG) will match 20% of annual contributions, up to $500 per year

These contributions can continue until you reach the lifetime limit of $7,200 per child

Investing your Canada Child Benefit can assist you while saving enough to qualify for the maximum CESG amount

Federal Government-funded education grants

The Government of Canada supports saving for a child’s education by offering grants to a child’s RESP – offering you additional funds to accumulate educational savings.

The Canada Education Savings Grant (CESG)

The basic Canada Education Savings Grant (CESG) increases your year by year contribution by 20%, up to $500 per beneficiary each year to a lifetime limit of $7,200 per beneficiary. Additional CESG grants may be available, depending on your income.

Please talk to us for more information about the RESP and the CESG grant as it applies to your province.

How parents help shape the financial future of their children

In Canada, the government allows a welcome tax break when you save for your child’s education. As parents, we need to consider the effect that education will have on the future income and lifestyle of our children.

The Internet is bringing many changes quickly: Amazon is replacing many of our once-renowned retailers. Google sweepingly controls business success: who gets to view your website and consequently buy your services is based on paying for Google AdWords. The world has moved into one of the most profound eras of change in human history. Our children, for the most part, are just not prepared for this new reality. The gap to accessing a secure income, or obtaining a job with a substantial retirement pension is widening.

Parents who can see the chaos, the economic uncertainty, the stress and the complexity in the world, know intuitively that the new wave of robotics and artificial intelligence (AI) call for an educational revolution. Our children must be able to get a post-secondary education while aiming for higher accreditation in a career known to provide substantial income that keeps up with inflation. Serious financial planning can provide significant funds to go to university or college. The Financial Comfort Zone Study found the following:

“Canadians who establish registered education savings plans (RESPs) for their children are setting their kids up for financial success later in life because there’s a direct correlation between having post-secondary education and wealth”.1

The study revealed the following:

• Among those holding a postgraduate degree (the highest level of education), 23% have investible assets of $500,000 or more, whereas approximately only 11% if the schooling is at the post-secondary level.

• Of those with only a high-school diploma, only 8% have investible assets of $500,000 or more, while 72% have investible assets of $100,000 or less.

Parents can influence the education of their children by fostering the right attitude toward the need for educational training for a financially sustainable future.

“Among parents who gave education a high rating of importance and who had one or more children living at home, 49% indicated they had established an RESP for their children. Similarly, 45% of parents who gave education a medium rating of importance and who had one or more children living at home indicated that they had established an RESP for their children. In contrast, only 15% of parents who gave education a low rating in terms of importance and who had one or more children living at home had established an RESP for their children.” 2

What ways can we plan for our Child’s education? Consider using both the traditional Registered Educational Savings Plan (RESP) and the Tax-Free Savings Account (TFSA) as an educational savings vehicle. A TFSA offers parents another tax-efficient method to provide for education planning.

The Canadian government regulates the Registered Retirement Savings Plan (RRSP) program, allowing it to have unique tax benefits as you save for your retirement. Annual RRSP contributions can reduce the amount of income tax you pay in the year of your contribution. These monies invested annually grow on a tax-deferred basis, and tax is only paid at the time of withdrawal. RRSP Planning is a very integral part of your investment planning.

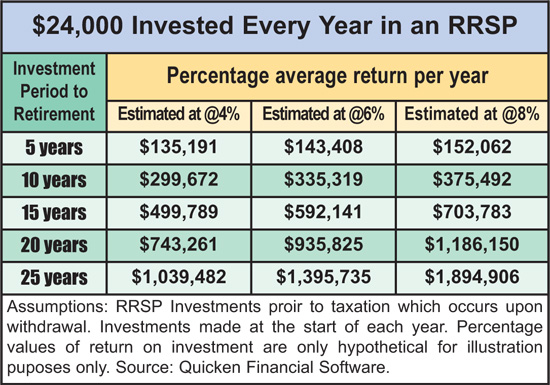

Have a look at the graph below to see how RRSP money accumulates over time based on a maximum annual investment.

Your investments grow tax-free Your RRSP investments accumulate within the plan tax-free, as do any addition to your contributions, including capital gains, interest, dividends, and any other growth via dividends or distributions paid out on an investment fund. The longer your money stays sheltered from the taxman, the greater the tax-free accumulative earning power of your investment. However, taxation occurs once income is withdrawn from your RRSP.

Planning Together – Spousal RRSPs and Tax

A spousal RRSP allows a couple to place assets in the lower-earning spouse’s registered account. The benefit of this manoeuvre enables the account owner to withdraw more in retirement at a lower tax bracket while retaining spousal RRSP ownership, controlling the choice of the RRSP investment vehicles. The owner also governs when withdrawals are made and pays the income taxes upon withdrawal (if the funds have been in the account for three years).

What happens when the RRSP account holder dies?

For estate planning purposes, upon the decease of the account holder, the RRSP is paid out to the beneficiary designated for that account.

How Much can you contribute to your RRSP?

Your Contribution Limit To find out your allowable RRSP contributions you are allowed to deduct for your income taxes, check Last Year’s Deduction Limit Statement on your latest Notice of Assessment or Notice of Reassessment. Canada Revenue Agency (CRA) establishes guidelines for the minimum and maximum overall yearly amount a person is eligible to contribute to their RRSP. The basic formula used to determine a taxpayer’s eligible contribution is as follows: 18% of earned income minus any Pension Adjustment = the eligible contribution amount.

Who can contribute to an RRSP? All Canadian taxpayers with “earned income” in the previous tax year, or those having unused contributions carried forward from previous years can contribute to their RRSP. A person is eligible to make contributions to their RRSP until December 31 in the year they reach age 71, provided that they have contribution room.

Two methods of contributing to your RRSP You may invest by purchasing a lump sum investment prior to the deadline. The alternative is to invest on a monthly basis using dollar-cost averaging. You can always top up your RRSP contribution (up to the allowable limit), just prior to the deadline year by year.

Fund managers usually diversify among at least 20 companies, investing no more than 10% of the fund’s total dollars into any one security.

Fund managers usually diversify among at least 20 companies, investing no more than 10% of the fund’s total dollars into any one security.