The insurer holds a reserve in relation to the several guarantees provided in the policy contract. Due to market fluctuations, it is especially important that actuaries calculate and hold reserves needed to pay any future liability due to a capital loss.

Guaranteed Capital Protection Because of the need to assess and insure the portion of capital guaranteed, insurers must be involved. A slightly higher management expense ratio (MER) pays for these capital-conserving features.

Retirement planning advantage Some segregated fund policies allow for additional insured security, promising that a pre-established monthly payment of segregated fund premiums (i.e., investments) will continue on your behalf in the event of a disability. Consider how valuable this pledge would be to your retirement if you could no longer work.

Many business owners focus on their business and must remember to invest seriously for retirement.

The Retirement myth of the Entrepreneur: Most business owners believe their company will provide investment capital when sold, or if passed on to the next generation, a salary or dividend payments. For some, their financial stability rides on the company’s future success.

Make hay while the sun shines. Don’t be overly optimistic that your company will succeed and create good revenue forever. Planning becomes necessary when a business represents an estate’s significant value. You may make hay while the sun shines, but be sure to stack a lot of it away for future use.

Many are not convinced that they need to plan their estate or the succession of their business. Despite the economic importance of their business, most business owners are still determining the tax liability if both spouses were to die. An estate plan can ensure that these taxes will be paid from one or a combination of the following sources:

Life insurance

The business, from cash flow or liquid assets

RRSPSs/RRIFs (taxed when both spouses die)

TFSAs

Sale of real estate or a significant asset.

Non-registered investments

We are all ageing despite our business successes. Please take the time to do some essential estate planning to figure out who will take over the company and where your retirement income will come from. Review your personal and corporate-owned life insurance, disability coverage, and key-person insurance. Revise or complete both your will and power of attorney.

In some cases, paying relatively small life insurance premiums can entirely solve the estate’s future capital gains tax problems or generate capital to replace the tax that may be payable in your estate. It is essential to purchase insurance currently versus when older or health declines. If your health is a concern, ask your life insurance specialist if he can search the market for you.

Life insurance can eliminate company debt and help a succeeding son or daughter with new business capital. Finally, it can equalise the division of your estate among all of your heirs.

Note: Life and disability insurance taxation vary in accord with the strategies used by the life insurance specialist, changing legislation, and hiring an accountant to guide effective business strategies relative to succession or an estate.

To know the state of your fiscal health, you must have a personal financial health check up. Your financial advisor will help put perspective on your diagnosis and how in shape you are for retirement.

Strategies can be designed to form a comprehensive plan to enhance your net worth as you move towards financial independence, secure in the knowledge that a retirement can become a reality secure with sufficient income.

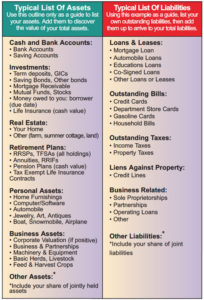

Your annual net worth statement is the benchmark measure of your ability to become financially independent. Net worth means the same as net assets – the assets you have left after you subtract your debts.

Why do this annually? Time waits for no one. Retirement approaches faster than most people admit. Consider how quickly the last five years has passed. Double this time back ten years to the 2008 financial crisis which woke the whole world to the need for financial guidance.

How can I know my net worth? Simply add up your liabilities compared to your assets. Subtract your total liabilities from your total assets to give you your net worth.

You gain awareness of your debts. Debt totals warn against spending beyond our means. Compound interest on a growing credit card debt at 18 to 28% can strain your cash flow. Always set goals to reduce debt.

Investment planning results become evident. Your net worth statement reveals all of your accumulated assets, including your RRSP, TFSA, and non-registered investments, putting them all into perspective. You may find that you need to rebalance your investments. You will also see which are performing well, suited to portfolio growth. While employed, this gives you a retirement metric concerning your future income goals to help you see how close you are getting each year.

It reveals opportunities for further financial solutions. Picture each financial need in contrast to your net worth snapshot. What have you saved for each future goal? Where has your income been going? Do you have home equity built up or do you still have a large mortgage? Is a Home Equity Line of Credit (HELOC) eating away at your assets? It can reveal the importance of keeping your credit cards paid monthly.

Estate & Tax Planning can affect your final net worth. To draft a will, you need to know your ultimate potential net worth inclusive of business assets. Identify capital gains tax liabilities or tax on a vacation property. Your registered monies (RRSP/RRIF) will be fully taxed after the death of the second spouse (in most cases). Assess the final estate tax liabilities on your assets now. Consider that life insurance offers the easiest solution for projected estate related tax debts.

Business planning can be enhanced. Succession planning simplifies the transfer of a family’s business assets to the next generation. Often a simple life insurance planning manoeuvre can ease the effect of capital gains tax or provide for a future buy-sell agreement upon the death of the principal business owner.

Getting into business is a lot easier than getting out. Many successful family businesses have accrued capital gains in the millions. The tax payable is so high that the business cannot afford the liability once the owner dies at least without liquidating.

One way to cover the tax liability is to save for it. The problem arises if the owner dies too soon, or the money gets used for an emergency or a new opportunity, or if the savings goal is impossible for the company to achieve.

A business owner’s retirement may depend on an estate plan.

Many business owners base their personal financial stability on the future success of the company. When a business represents the major value of an estate, planning becomes necessary. Yet, many are not convinced that they need to plan their estate or the succession of their business.

Find out what your tax liability will be. Despite the financial importance of their business, most owners do not know what the tax liability would be if both spouses were to die. An estate plan can ensure that these taxes will be paid from one or a combination of the following sources:

· Life insurance.

· The business, from cash flow or liquid assets.

· RRSPs (also taxed when both spouses die).

· Non-registered investments.

Frequently review your capital gains tax liability. In some cases, the payment of relatively small life insurance premiums can entirely solve the estate’s future capital gains tax problems, and/or generate capital to replace the tax that will be payable on your RRSPs when both spouses die.

When you buy life insurance it immediately covers the entire estimated liability risk, which is due. The benefit is paid upon the owner’s death (or the death of a surviving spouse).

Put succession planning on your agenda. Consider taking the time to do some succession training when you are active in the business, passing on what you know, while unifying current action with your estate plan. Sometimes successful business owners, while waiting for the perfect person to take over, run out of time.

Determine who will take over the company. If you are a family member, an employee, or a competitor, you will need to begin negotiating with your successor(s). Income from a good succession plan may nicely increase your retirement income. Therefore, it is good to know where it will come from.

Keep your legal documents current. Revise or complete both your will and power of attorney. Review your personal and/or corporate-owned life insurance, and disability coverage.

Establish or update your buy-sell agreement. Make sure your buy-sell and key-person agreements and applicable life insurance, is current and sufficient to cover your succession plans.

Other uses of new business capital offered by life insurance. A sole owner may buy enough life insurance to add capital to offer additional financial stability where a wife, son, or daughter goes through the transition to actually run the business. Insurance can also eliminate company debt to give a succeeding son or daughter a fresh start. Finally, it can fairly equalize the division of your estate among all of your heirs.

Life insurance has provided families with basic financial security for well over 100 years. For example, a healthy, non-smoking 40-year-old male can purchase up to $500,000 worth of insurance for approximately $50 per month. That life insurance policy would pay out a death benefit, the equivalent of up to 10,000 times the amount of one monthly premium payment.

In this case, the $500,000 could provide necessities such as groceries, shelter, home repairs, means of transportation, and education for dependents. In this sense, the value of life insurance is tangible. Contrasted against the assets and services such a large death benefit can purchase, we realize how small the premium cost really is.

When does life insurance begin covering my family’s financial risk?

Even if death occurs one day after the initial premium payment, the full benefit is payable tax-free, thus instantly creating new capital, sometimes far exceeding the insured individual’s net worth. Most accountants and financial advisors agree that life insurance is foundational for families with dependents to build financial security.

An immediate foundation of financial security. In addition to savings, life insurance is designed to immediately provide the capital necessary to create ongoing investment income for dependents after income taxes and other liabilities are paid.

When you are not financially independent Life insurance can make up the shortfall when investments assets have not yet grown to the extent that your net worth enables you or your heirs to live in total financial independence.

When your health is not the best Many people who are not in perfect health are surprised to find that they can also purchase life insurance to ensure their financial security.

Note: Life insurance premiums vary according to the policy type. In some cases, paying a little more premium offers enhanced benefits Be aware that tax-deferral strategies may change due to legislation.

One way to cover the tax liability is to save for it. The problem arises if the owner dies too soon, or the money gets used for an emergency or a new opportunity, or if the savings goal is impossible for the company to achieve.

One way to cover the tax liability is to save for it. The problem arises if the owner dies too soon, or the money gets used for an emergency or a new opportunity, or if the savings goal is impossible for the company to achieve. Frequently review your capital gains tax liability. In some cases, the payment of relatively small life insurance premiums can entirely solve the estate’s future capital gains tax problems, and/or generate capital to replace the tax that will be payable on your RRSPs when both spouses die.

Frequently review your capital gains tax liability. In some cases, the payment of relatively small life insurance premiums can entirely solve the estate’s future capital gains tax problems, and/or generate capital to replace the tax that will be payable on your RRSPs when both spouses die.