The risk/reward concept states that the higher the risk of a particular investment, the higher the possible return. Although there is usually risk with any equity investment, assessing just how much risk your portfolio should carry is essential. Risk involves the potential for gain or loss of monies invested.

Many people take on more risk, hoping to achieve a higher return without regard to cyclic markets. If an investor expects higher returns based on the past, he must understand that markets can go through gain and loss periods.

In theory, many think that the higher the risk, the more you should receive for holding the investment. With cyclic markets, this is not necessarily true. Conversely, in theory, the lower the risk, the less you should receive. Unfortunately, the dilemma is this: a higher potential for above-average returns comes with a higher risk of below-average returns. Conversely, safer investments, such as cash and bond instruments, have a lower potential for high returns and a higher potential to not keep up with inflation.

While choosing investments for your portfolio, you need to be conscious of risk/return trade-offs and risk tolerance. Different types of securities have associated levels of risk. Every investor’s goal should be to find a balance that allows you to not experience undue anxiety in the markets and achieve your long-term financial goals at the same time.

Psychological fear can hold one back from investing. People behave according to their mindset. Some of the following thinking can keep one from not putting their money to work by buying equity investments such as equity investment funds. If you have said any of the following statements, you may be experiencing investor anxiety:

“I think the markets will pull back and lose some value.” I will wait and invest when this happens.” This viewpoint is based on the need to confirm a belief before acting, where the investor must minimize any evidence that contradicts their belief mantra. The media frequently offers terrible news if the market has a low day, and it is easy to hear only this information while filtering out other positive news. This process can paralyze an action plan to invest for years.

“I want to sell the investment if I see a profit.” People might sell an investment early once it rises in value for fear of future loss. Aside from considering taxation, once sold, an investment with either a gain or a loss ends any future potential of that investment rising in future value. To avoid this mindset, one should have a disciplined written plan for buying and selling assets that can be frequently referred to.

“The market is bound to correct and head down because it is at a peak.” Anchoring our point of view occurs when someone assigns a reference number, like a 52-week high or low, to compare the price of an investment stock, the unit value of a fund, or a stock exchange’s last peak value. Past price movements are poor predictors of future price performance. When you invest for the long-term for retirement, using past price patterns is comparable to driving your car while gazing in the rearview mirror as a reference.

Conclusion

The above emotional mindsets can ruin or avoid forming an otherwise excellent investment plan. They can help you develop a risk tolerance profile and investment plan. Please work with your investment advisor to help you understand how the mind can trick us into failure simply by not investing over the long term.

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.” Benjamin Graham

What are the key insurance components of an Estate Plan?

An estate plan is a singular categorical part within organized financial strategies aimed at achieving financial independence. Life insurance, disability insurance (group or personal), critical illness (CI) insurance and long-term care (LTC) insurance policies are key components of a good estate plan when protecting your family’s financial security.

Keep your documents up to date with your life needs. It is important that an individual maintains and updates a will and two powers of attorney documents: 1) for property such as real estate, bank accounts, and investment assets, and 2) a power of attorney for personal health care.

Life changes can affect the integration of each of the above strategic solutions. Therefore it is important to review the above aspects of an estate plan every three to five years. For example, there may be a change in the beneficiaries, where a person needs to be added or removed during an addition to the family; or if you remarry, your existing will may automatically become nullified.

There may be significant changes in your net worth if the value of your residence or investment assets change over time; or your liabilities increase or are paid off. If you have significant assets, have your accountant make sure that the best tax arrangements are in place.

Business owners If you are the shareholder of business assets, make sure that a buy sell agreement is in place in the event of your death or disability, assuring that every owner is covered with life and disability (income replacement) insurance.

An estate plan may benefit from using formal trusts to reduce taxes and segregated funds to circumvent or minimize probate or estate administration tax and/or fees or protect assets from creditors.

Life insurance with named beneficiaries can also be solutions to transfer capital tax-free to heirs outside of probate/EAT scrutiny. For an estate plan seeking to transfer large capital assets to named heirs, it would be wise to discuss these capital-transfer techniques with an account and/or tax lawyer.

Estate planning provides some ability to minimize the obstacles that loved ones might encounter in the event of an unexpected death such as:

Fear of losing your money by erosion of capital that might come about with poor investments.

Delays during the settling an estate can be a lengthy process.

Legal and accountancy costs, probate fees, and taxes.

Potential liabilities for Executors and Trustees in Ontario re the new administration of probate/EAT in 2013.

Lost privacy due to your will becoming public during the probate process.

Ability of your beneficiaries to handle money as some children are less capable than others of handling large amounts of money

How can the use of Segregated Funds and Term Funds help?

Ability to invest in diversified funds that have professional money management to help your clients preserve their capital.

Segregated funds and Term funds with named beneficiaries can avoid probate, making payout quicker.

By avoiding probate, your wishes are kept private.

There are excellent estate planning concepts such as the Gradual Inheritance concept that can help you better plan the allocation of money to your children (eg., buying an annuity or deferring payout until the child turns a certain age)

A good financial advisor will not only assess your current fiscal resources. They will also outline a plan to achieve your goal for a sound financial future.

As time passes, so does your opportunity to build a solid financial future. Suppose you are to develop an investment portfolio and a significant net worth. Will you personally determine how to purchase stocks among the international markets, analyse investment funds, and sidestep economic pitfalls as you invest all by yourself? Will your financial stability be based on our government’s pension plan? Did you know that its maximum benefit covers only 25% of the average Canadian’s wage?

Why involve an advisor in your financial affairs?

The majority of Canadians seek specialised professional help. Their work is to guide you towards achieving financial independence. An advisor’s work is to help you systematically achieve your goals and make your life dreams come true.

• An advisor must analyse your current financial resources to define appropriate financial strategies that are best suited to your current and future personal priorities, retirement goals and risk tolerance.

• Calculating your current net worth and cash flow after taxes is also essential. With a net worth statement, a financial specialist can identify any opportunities or problems relating to capital gains, life insurance, disability, and critical illness insurance needs versus your present coverage, investment growth, income taxation, retirement income needs, employee benefits, and potential capital gains tax liabilities for your estate. Parents must also assess educational funding needs and plans for any dependent adult child and special health care such as Long Term Care (LTC) for parents.

• Establishing a written plan sets forth specific solution-oriented recommendations and will enable you to see how ordering your finances can benefit your overall lifestyle.

• To achieve your goals and objectives, acting on the plan’s recommendations will be necessary. Building a solid portfolio of investments tailored to meet your goals and risk tolerance is essential for your future financial independence.

• Appropriate life and disability insurance coverage will ensure your plan meets family income needs, business debt or buy-out payments, and any tax liabilities for your estate.

• Finally, an advisor will establish a periodic review to monitor and refine your plan to accommodate birth, marriage, illness, or retirement events.

There are specific life insurance policies offered with attractive tax-planning advantages. Legal tax-exempt rights are allowed in our tax legislation with life insurers, enabling the possibility to accomplish the following.

Premiums over and above the associated costs of insurance and premium tax are invested and can accumulate tax-deferred within specific plans.

Tax-deferral of the investments continue until such time that withdrawals are taken out from the policy.

Tax is avoided on both the face amount of the insurance and any ongoing cash accumulation in the policy when paid out to the beneficiaries on the insured’s death.

Taxation details. Most of the cash received from a life insurance contract is not subject to income tax. 1 Your beneficiaries — spouse, children, grandchildren or other beneficiary allocated will not need to report life insurance benefit proceeds on their tax return as taxable income. However, if you have assigned your estate as the beneficiary, the death benefit could be subject to tax. Moreover, fiscal gifts or inheritances generally are not taxable.

Beneficiaries or heirs do not owe estate inheritance tax or death tax. It is the estate of the deceased that pays any such tax due to the government. If the policy owner’s estate is the policy’s beneficiary, the death benefit may — in some cases be subject to tax. 2

When could a taxable situation arise?

When you own a permanent life insurance policy, accumulating interest or equity investments made to a policy’s cash value, taxes will be payable on that growth gained above the cost base of money invested. 3

Upon your beneficiaries receiving any investment earnings from the policy, along with a death benefit, the increase on investments, not the death benefit, would be taxable as income.

Likewise, you will pay taxes on any increase in cash value based on the investments in the policy fund — should you surrender the policy and receive its cash value in return.

Tax Reporting Rules for Life Insurance Payouts

The Canadian Revenue Agency (CRA) makes receiving life insurance proceeds easy for beneficiaries relative to tax reporting. Unless the tax is due on the above-stated earnings, these amounts do not need reporting as taxable income on a tax return.

What if there is an increase in the cash value?

These amounts don’t need reporting as taxable income on a tax return unless some tax is due on interest earnings. If there are interest earnings, it will be reported to the beneficiary by the insurance company on a T5 slip, reportable on line 121 of the beneficiary’s return (or of the policy owner when surrendering the cash value of the policy). 4

Here are some uses within an estate:

Final tax liabilities in an estate such as on capital property or the remaining RRSP/RRIF value is taxed fully as income and can be pre-funded.

In some cases, tax-exempt plans are used as a pledge to secure a loan to create additional cash flow in retirement. Cash resulting from a loan is not taxable. Where the loan is later paid from the death benefit, payment can be deferred until death. Repayment of the loan is thus partly repaid using pre-taxed dollars.

Others may borrow directly from their policy subject to the policy terms.

Estate Planning is a financial planning process that every responsible working person with dependents should accomplish, even if it is preparing a last will and testament and living will for health purposes.

Estateplanning can empower your heirs in the following ways:

Plan to reduce taxes in your estate When transferring your assets, including mutual funds, using a will, try to pass as much value as possible to your heirs. If you hold equity mutual funds that buy and hold stocks, they may have accrued capital gains. There will be a deemed disposition of all your property at fair market value at the time of your death. For some this could mean a capital gains tax liability.

By knowing your estate tax liability List each separate asset you own, the purchase price and date, as well as its current value. Include your non-registered investments in stocks, bonds, and mutual funds. Have your accountant assess what the tax liability will be.

Your spouse and deferred taxes Property willed to your spouse can be rolled over tax-free on your death. Your spouse will actually inherit the assets at the unchanged adjusted cost base (cost amount) of the property. The taxation of the asset will then occur when your spouse disposes of the property or at the death of the spouse. This tax deferral is beneficial especially if you have large holdings in equity mutual funds invested for value as in large cap or blue chip stocks. Alternatively, you can choose to transfer any asset to your spouse at fair market value on death and recognize the accrued gain or loss.

RRSPs and your children Under the rules proposed in the 1999 Federal Budget, RRSPs can be transferred tax-deferred to your dependent children or grandchildren, even if a spouse survives you. Before the 1999 Federal Budget, a transfer of RRSP funds to dependent children or grandchildren would be taxable if there was a surviving spouse.

Income splitting using a testamentary trust By establishing a testamentary trust in your will, you will be able to maintain control during your lifetime over the use of your assets such as a mutual fund investment portfolio. The trust can provide guidelines for the treatment of these assets after your death. The trust document can specify the split of income among heirs. Carefully planned income splitting may allow for significant tax savings.

Assess your tax liabilities with an estate lawyer and/or accountant and make estate plans to determine how to pay them. Consider the use of life insurance where the capital gains tax liabilities are substantial.

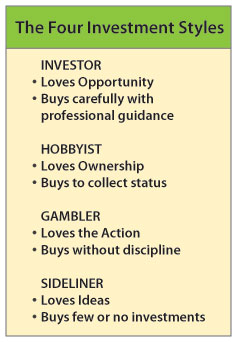

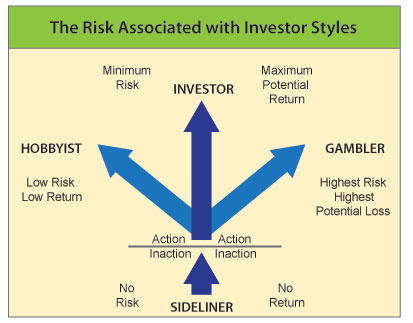

There are four basic types of people, each with differing mindsets when they approach investing; the Sideliner, the Gambler, the Hobbyist, and the True Investor. If you want to be a serious and successful investor, you must mindfully recognise the erroneous attitudes of the Sideliner, the Gambler, and the Hobbyist.

The Sideliner Sideliners are fearless in taking action as long as they are in the audience and won’t ever get bruised. They shout, stand, and clap, loving the action of a bystander. Sideliners love the excitement of stock market news and the investor’s game. They often look at how the indices, a stock, or a fund performed. Observation alone never gets you in the game of investing. Sideliners may feel it is dangerous in the arena of the investor.

The downside Sideliners are analytical and love running numbers hoping to reduce most risk by comparing return percentages. Yet, out of the paralysis of information, fear sets in, and they make minimal purchases to play it safe. The sideliner is a silent observer possessing discernment for weighing facts, yet witnesses other people’s investment success without taking action to enjoy investing personally.

The Gambler These people are confident thrill seekers who enjoy the casino, horse race, or scratch-and-win tickets, unlike the Sideliner. They confuse play gambling with risk tolerance, spend recklessly, consider that investment principles are for misers, and don’t seek the guidance of an advisor and consequently have a retirement portfolio that looks broke.

The downside The Gambler is comfortably numb and usually gets punished with frequent losses for taking above-average risks. They might buy an investment based on listening to the talking heads in the trading media, buy penny stocks, or low-priced failing company stocks — all based on uncredentialed hearsay. Because they think they might make some fast money, they believe they are investing but are not. Rarely does a Gambler stay invested for the long term.

The Hobbyists They buy things and investments based on their emotional value more than on investment value. As collectors, they buy for popularity status, notions of status, aesthetic gratification, and pleasure.

The downside Hobbyists, when excited, may jump to buy anything referred to them by word of mouth or a talk show host. They may own all the British Royal plaques on a wall or the top “500 must-see movies before you die”. Financial perspective gets lost because several investment funds may be bought by virtue of historic popularity instead of the potential for future gains. Because collections have been known to go up in value, they think they are investing. They do not understand the old Latin proverb “Non Quantum Sed Quale”, meaning it is not the quantity but the quality that counts.

The True Investor Utilizing an advisor’s wisdom, they buy suitable investments. Unlike Sideliners, they act. Unlike Gamblers, they minimise risk. Unlike Hobbyists, they buy based on investment value.

Investors are defined by their knowledgeable expectation for financial gain employing a principled process to minimise financial risk. Many also make it their practice to utilise professional managers and advisors when investing.

Actual investors act with a vision to achieve excellent returns on their investments while exposing themselves to mitigate the risk that suits their investor profile while enjoying the actions that lead to real financial success. It all comes down to how you think and whether you’re considering investment action.

Since the 1920s the ratio of seniors over the age of 85 has doubled to one out of every 10 people. This number is to increase, to five times the current demographic, into the 2050s. That means that half the population in 40 years will be over age 85.

Who will care for you in your old age? When our health is fine, it is hard to imagine that we may as many will, lose the ability to manage our basic daily activities such as bathing, toileting, walking, dressing, feeding, or moving from our bed to a chair. Many also lose mental faculties that we often take for granted such as memory, logical or conceptual thinking or referencing dialogue with others. Without assistance it is near-impossible to function without these capacities.

Long-Term Care Insurance (LTCI) is an insurance contract with an insurer that is designed to provide care for our own chronic illness, disability, or an accident, all which have a higher potential of occurring as we age.

Some families are incapable of caring for a senior LTCI protects our families from the financial strain of providing long-term care, just as importantly as life and disability insurance protect the income of younger families. The ultimate question is who will financially support long-term care for you? LTCI is not just for seniors but for those who become similarly incapacitated at any age.

It is important to independently plan for our own long-term care because our government healthcare budgets and initiatives are limited. Facilities are often understaffed with overworked or burned out employees. Strict regimes are often the norm where the government foots the bill in both government- and privately- run institutions (many private companies provide government-funded care). For example, bathing can be limited to twice a week, toileting to three times a day, elders may not allowed to take a nap, and most are all placed in bed at 8:00 pm to be awakened to prepare for breakfast at dawn. These are the governmental necessities where a limited budget provides extensive health care for the aging populace.

The majority of us understand the need to save for retirement that can provide an income sufficient to meet our lifestyle expenses. However most people entirely overlook the enormous expense of paying for a private long-term care facility (some cost up to a quarter of a million dollars for five years). Why are they so expensive? They offer 24/7 high-level nursing care in a highly secure environment. Note: Anyone can call a few private long-term care companies and inquire about the cost for their care.

The time is fast upon us when aging baby boomers starting to retire will increasingly depend on long-term care, either paid for by themselves, their children and/or professional health care services.

If you are a business owner, you may have an individual critical to your success. Insurance can protect you against financial loss if incapacitated in three areas.

1) Key-Person Life Insurance

2) Key-Person Critical Illness Insurance

3) Key-Person Disability Income Protection

Key-Person Life Insurance Life insurance is usually the foundation of a key-person protection strategy. It provides an immediate injection of capital into the business precisely when needed—when a key person dies. At this time, the death benefit is paid to the company tax-free.

Renewable Term Life Insurance is usually the most economical option over the short term. In certain circumstances, permanent insurance may provide better protection when coverage is needed over a long time.

Key-Person Disability Income Protection Disability insurance can be used for two purposes in a key-person context:

• The provision of a continued salary to a key person that becomes disabled, usually until the earlier of age 65 or recovery from the disability.

• Owner-managers can purchase insurance that provides continued payment of office expenses and salaries during disability, usually for a limited period.

Key-Person Critical Illness Insurance Critical illness insurance provides protection when a key person is afflicted by a specified disease or health problem that does not necessarily render them disabled but affects their desire or ability to work. Depending on the policy, this insurance coverage can pay a lump sum, or an income payable to the business, to help cover losses created by the absence of or lower productivity of the individual.