One thing is true about building wealth. The discipline of spending less money is the surest path to saving more. But you may have to reform your thinking—we do not deserve to buy something now if we can’t afford it today. Here are a few suggested ways to help you spend less:

• Shop with cash. If you carry a debit or credit card, it is too easy to escalate your buying when out at the mall. Better to put a budgeted amount of money in your pocket and spend no more—make sure you include enough for a treat at the café.

• Clean your clothes at home. Try to buy clothing that can be washed at home, using caution not to shrink your fabrics.

• Don’t fire up a temptation. Don’t bother browsing the catalogues, the clothing racks, or the car lot if you don’t have an honest need.

• Look for freebies. Avoid all the little service charges that hotel chains are starting to slip onto your invoice. Try to include extras with your vacation packages. Buy vacations in domestic dollars if you can. Plan to attend one of the numerous festivities municipalities pay for and provide in the summer holidays. Consider that many entertainment venues offer discounts just before the show.

• Borrow DVDs and CDs at the library. Try your library for movies or music—you may be surprised by their free access. Many have shared password to streaming services such as Netflix though they are clamping down on these methods.

• Take portable picnic coolers to avoid eating out. This can save you hundreds of dollars per month. Picnics are great getaways in the summer and can be carried in coolers in your car.

• Learn the skill of cooking. You can add artistry and relaxation to your fine dining experience by learning to cook. It is easy to rack up over $50 or more with a tip when two eat out. Consider splitting larger meals with your partner when you go out on the town. Avoid supersizing fast food, which may cost more, and add calories.

• Limit prepaying your taxes. Adjust your income tax deductions at work to ensure you aren’t pre-paying too much.

• Do a “needs analysis” by asking, “Do we need it?” Make lists and discuss your actual needs. This is where your partner can help you be honest and accountable by simply discussing every purchase, at, say, over $50—set your dollar figure at a point where you involve the other’s advice.

• Liquidate if you have too much stuff. Space costs money, so consider what is essential. Go over your furniture, books, and general stuff, to determine what you don’t or won’t use in the next five years. If you don’t love it, sell it, or give it away.

• Invest your raise. Avoid spending up to any increase in your income. Instead, plan to invest it.

• Assess the unit price and buy in bulk. Everything is sold in quantity and can be compared with a competing brand by ounce, kilo, serving, etc.

• Buy depreciated cars. Buy vehicles used after a year or two with the factory warranty still on them. Avoid the most significant depreciation that occurs among assets.

• Reduce your vehicle’s weight. Unload excess vehicle weight that can cost gas or battery (with an electric vehicle) consumption. Similarly, having your tires carry the correct PSI will offer better gas mileage.

• Know that it all eventually goes on sale. It makes sense to wait it out for the seasonal sales. Stores often begin to sell their seasonal stock, including clothing, before the need. So if you are savvy, mark the best times to buy in your calendar. This is also true of travel bargains.

• Pay cash only for groceries. Have you ever spent double what you intended on items that can be eaten? If you pay money, you are forced to budget regardless of your hunger, sticking to the necessary things.

• Know where the quality brands are. Don’t purchase items that will wear out prematurely and have to be replaced; instead, buy quality, but shop around for the best prices.

• Buy more when it is cheap. If you can buy tuna, salmon or spaghetti at 30% less than usual, why not stock up on it? But don’t buy multiple “on-sale” items if you don’t need higher quantities.

• Make fun fast food. You can make fast food, such as fruit or vegetable trays, for drives, hikes, or stay-overs.

• Use public transit. By not driving all the time, you may save some money. Many municipalities offer cheap bus or train transportation. Some prefer not to go if they live in a large city such as Vancouver or Toronto. There are car-sharing co-operatives in larger cities. They can mitigate insurance, fuel, and repair costs on top of any lease or loan payment (along with interest). Car rentals can be cheaper in the winter and on weekends.

• Cut your hair between significant cuts. Sometimes a minor home trim will add another week before you must visit the barber or hairdresser.

• Utilize the secondary market. Most of the world’s literature is available online for under $5 for the entire life-work of an author, sold on Amazon Kindle. If you are a bookworm, Amazon.com or Abebooks.com may help you find the book; or perhaps find a camera on eBay at 50% off the cost.

• Make the park your gym. Why not walk around the park’s pond and get outside as a bonus?

• Adjust your thermostat. You can save a few hundred dollars per year by juggling temperatures by one to two degrees on your thermostat (wear sweaters or shed clothing).

• Know how and when to return merchandise. Ask about return policies when shopping. Many admit mistakes or displeasure with a product and promptly return it according to policy—in the free market, that is more than fair! Often it is wise to reassess a purchase in a day or two.

• Pre-pay certain vacation costs. Prepaying for a resort food plan in domestic dollars to avoid paying later for dollar-exchange loss can make budgeting sense because you’ve got to eat anyway. Likewise, prepaying museum ticket passes can save money and side-step long lineups.

• Stop—don’t shop! Tell yourself to stop shopping when you have no imminent need. Try walking, sitting in a café or reading instead.

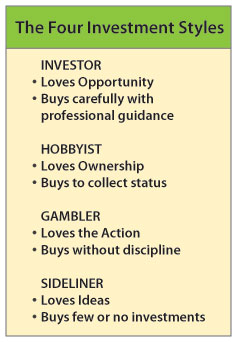

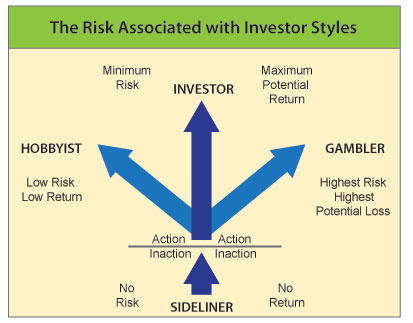

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?