Here are several tips to contemplate before investing in a mutual fund:

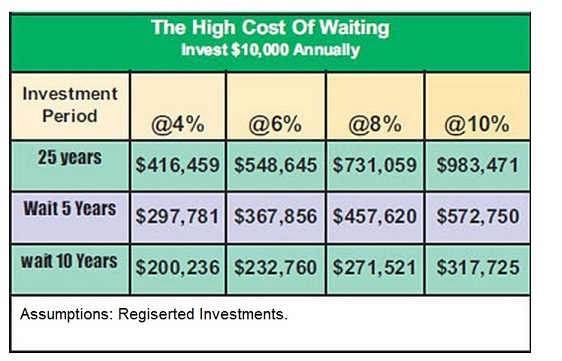

1. Eliminate the unreasonable desire for get-rich-quick profits. No one gets rich overnight after purchasing mutual funds. However, many people may get rich investing in them over the long term (at least 5-10 years). Equity funds (those holding stocks) are affected by the stock market when the market is gaining and when it is depreciating.

2. Identify your investment goals. Will you be saving for your child’s education over 15 years, or investing for retirement over 5, 10 or 20 years? Don’t buy a fund just because it has skyrocketed in value during any one period. Instead, choose the fund most suitable for your investment purpose. For example, keep short-term investments liquid if you put money away for an emergency (it is advised to save three months of income for costly emergencies). You can use a money market fund for this saving, not an equity fund. Consider using equity funds for a more extended investment period of 5-10 years.

3. Invest in several types of funds. Don’t put all your money in one fund basket. A well-rounded fund portfolio utilizes several investment types of securities: equity, balanced, bond, and money market funds, for example.

4. Maximize your tax savings. Register a mutual fund investment (to create an RRSP) if you do not yet own an RRSP. Contributions are tax-deductible in relation to your taxable income, and the investments grow tax-deferred.

5. Position your fund investments. The best place for retirement investments that accrue interest or generate high returns is inside your RRSP because the income on these investments won’t be taxed year by year. Thus, you will gain the advantage of the total yield without the tax on interest-as-income. If you earn 5% and pay 40% in tax, you’ll only get 3.0% in a non-sheltered, non-registered investment (in the RRSP, you’ll get the full 5%). Consider placing mutual funds that accrue capital gains and pay dividends over fewer taxable distributions in a non-registered vehicle or a Tax-Free Savings Account (TFSA).

6. Invest in yourself first. The advantage of owning mutual funds is that you can establish a plan where the money is automatically taken out of your bank every week or month and invested (by purchasing fund units). You probably won’t miss this portion of your pay; try to invest 10-20% of your paycheck using this method.

7. Take investing seriously. Investing is that act of life whereby you put away today what you will need tomorrow.

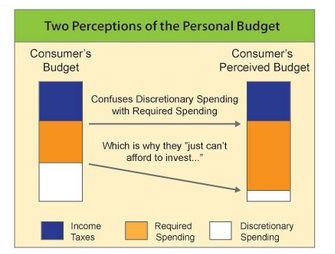

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?