Statistics Canada releases inflation figures regularly to determine the health of the Canadian economy. Increasing inflation indicates that the economy’s overall prices are rising. On the upside, this means there is good economic growth pushing these numbers higher. Some inflation is necessary to a vigorous economy. Fast increases in the index percentile can spark the Bank of Canada to raise our interest rates to keep the costs of goods and services in check.

When you go to the pumps or to the grocery store, ask yourself, “will my retirement investment portfolio create sufficient income to pay for all these rising expenses?” Only by accumulating assets in your pre-retirement years, will you be able to increase your net worth, which can lead you to financial independence. The cost of our basic retirement needs will increase.

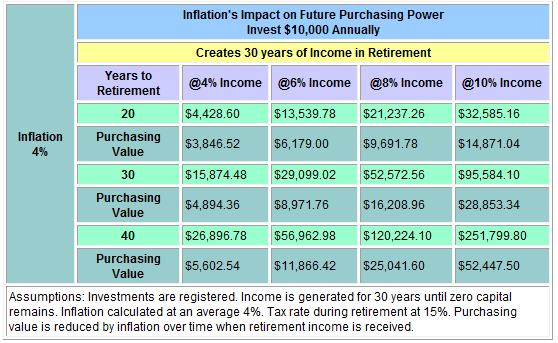

Investing to beat Inflation is a constant battle.

The importance of the economic fact of inflation may not be obvious. “What does the fish know about the water in which it swims?” asked Albert Einstein. Over the years, inflation has radically reduced our buying power. Interest rates when increasing as a policy to combat (reduce) inflation can also increase our debt repayment load as a percentage of income putting a strain on our budgets. In this respect, both inflation and interest on the debt are the foremost enemies of wealth creation.

How inflation is calculated Canada’s national statistics are weighted to reveal increases for the basket of goods and services in the Consumer Price Index (CPI).1 Consumer spending patterns for 12 months up to October 2021, can be seen by visiting Statistics Canada.

Three of the eight major components saw unprecedented growth in their basket weights, the statistics agency said, led by shelter representing soaring house prices during the pandemic–the highest-weighted major component, which grew to 30% as a share of the basket. The share of the household operations, furnishings and equipment component grew to 15.21% and alcoholic beverages, tobacco products and recreational cannabis went up 4.86%. The Bank of Canada targets overall weighted inflation at 2%, with a 1%-3% control range. 2

You can get ahead of inflation now by investing. A healthy investment fund portfolio can give you a sense of financial security, earned by continued discipline and adherence to the principle of saving, which adds to our sense of personal dignity.

Saving on a month to month basis while purchasing investment fund units can help you realize your goals and objectives in life (such as acquiring a home, making major purchases, travelling, putting children through college or university, or going back to school yourself). Finally, your investments must outpace inflation—the rising cost of goods and services—the investor’s worst future enemy. Ask your financial specialist to do a complete analysis of your retirement income potential.

1 StatsCan

2 Reuters

There are many funds to choose from.

There are many funds to choose from.

Mutual Funds allow the investor the same access to securities as the institutional investor—access to stocks and bonds from many different companies. Moreover, mutual fund investments can gain the tax-advantaged benefits if they are registered in one or more of several savings plans offered by the Canadian government.

Mutual Funds allow the investor the same access to securities as the institutional investor—access to stocks and bonds from many different companies. Moreover, mutual fund investments can gain the tax-advantaged benefits if they are registered in one or more of several savings plans offered by the Canadian government.

A charitable contribution is a gift, and, like any gift, is an irrevocable transfer of a donor’s entire interest in the donated cash or property. Hence the donor’s entire interest in the donated property is transferred, and it is for the most part (except for “designated” uses) impossible for the donor to recover the donated property.

A charitable contribution is a gift, and, like any gift, is an irrevocable transfer of a donor’s entire interest in the donated cash or property. Hence the donor’s entire interest in the donated property is transferred, and it is for the most part (except for “designated” uses) impossible for the donor to recover the donated property.