The following advantages, make investing in mutual funds simple:

· Simplified investing You can select an industry or sector or country and/or currency within which a mutual fund trades securities. You do not have to to hand-pick each security. The mutual fund manager does this security selection process for you. You don’t have to be assessing which stock or bond may or may not be a winner. A fund manager is trained to weigh out all the market contingencies which can affect investor performance.

· Low-cost diversification A small monthly purchase plan can have you moving forward in your mutual fund investments in a day. Your money can buy a piece of many different investments held within one or more funds.

· Dollar-cost averaging Dollar-cost averaging allows you to buy more fund units when the unit values are down, less when they are high, giving you some benefit from downward volatility.

· Flexible access to your money You can sell your fund shares in one day. Your proceeds are available the next day if your money is needed in the short term.

· Portfolio balancing Choices include the full range of fund types, and strategies are available to use such as strategic balancing of your fund holdings.

· Automatically invest You can automatically invest more in mutual funds at any time or use dollar-cost-averaging.

· Professional management Mutual funds have active professional management watching over your investment.

You may want to consider using segregated funds when the market is offering low snail-paced returns on guaranteed term deposits.

The following advantages, make investing in segregated (seg) funds simple:

Invest in stocks when interest rates are low Interest rates on term deposits pay a very low percentile return per year, whereas the stock market can grown rapidly.

Simplified investing You can select an industry or sector, for example, without having to hand-pick each security. The segregated fund manager does this selection process for you. You don’t have to be assessing which stock or bond may or may not be a winner. A seg fund manager is trained to weigh out all the market contingencies which can affect investor performance.

Low-cost diversification A small monthly purchase plan can have you moving forward in your segregated fund investments in a day. Your money can buy a piece of many different investments held within one or more funds.

Dollar-cost averaging Dollar-cost averaging allows you to buy more seg fund units when the unit values are down, less when they are high, giving you some benefit from downward volatility.

Flexible access to your money You can sell your seg fund shares in one day. Your proceeds are available the next day if your money is needed in the short term.

Portfolio balancing Choices include the full range of seg fund types and strategies which are available to use such as strategic balancing of your funds holdings.

Automatically invest You can automatically invest more in segregated funds at any time or use dollar-cost-averaging.

Professional management Segreaged funds have active professional management watching over your investment

Segregated funds also offer some certainties Some guarantees are offered or optional as far as principal retention goes or the investor, which are quite different than segregated funds, which may differ according to the segregated fund policy.

Talk to your advisor about how you might benefit from the use of seg funds in your investment planning strategies.

Psychological fear can hold one back from investing. People behave according to their mindset. Some of the following thinking can keep one from not putting their money to work by buying equity investments such as equity investment funds. If you have said any of the following statements, you may be experiencing investor anxiety:

“I think the markets will pull back and lose some value.” I will wait and invest when this happens.” This viewpoint is based on the need to confirm a belief before acting, where the investor must minimize any evidence that contradicts their belief mantra. The media frequently offers terrible news if the market has a low day, and it is easy to hear only this information while filtering out other positive news. This process can paralyze an action plan to invest for years.

“I want to sell the investment if I see a profit.” People might sell an investment early once it rises in value for fear of future loss. Aside from considering taxation, once sold, an investment with either a gain or a loss ends any future potential of that investment rising in future value. To avoid this mindset, one should have a disciplined written plan for buying and selling assets that can be frequently referred to.

“The market is bound to correct and head down because it is at a peak.” Anchoring our point of view occurs when someone assigns a reference number, like a 52-week high or low, to compare the price of an investment stock, the unit value of a fund, or a stock exchange’s last peak value. Past price movements are poor predictors of future price performance. When you invest for the long-term for retirement, using past price patterns is comparable to driving your car while gazing in the rearview mirror as a reference.

Conclusion

The above emotional mindsets can ruin or avoid forming an otherwise excellent investment plan. They can help you develop a risk tolerance profile and investment plan. Please work with your investment advisor to help you understand how the mind can trick us into failure simply by not investing over the long term.

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.” Benjamin Graham

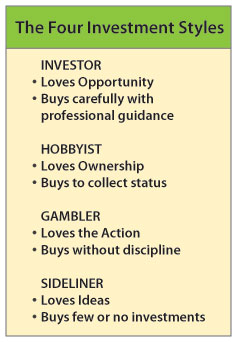

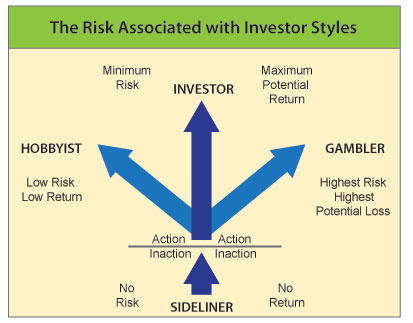

There are four basic types of people, each with differing mindsets when they approach investing; the Sideliner, the Gambler, the Hobbyist, and the True Investor. If you want to be a serious and successful investor, you must mindfully recognise the erroneous attitudes of the Sideliner, the Gambler, and the Hobbyist.

The Sideliner Sideliners are fearless in taking action as long as they are in the audience and won’t ever get bruised. They shout, stand, and clap, loving the action of a bystander. Sideliners love the excitement of stock market news and the investor’s game. They often look at how the indices, a stock, or a fund performed. Observation alone never gets you in the game of investing. Sideliners may feel it is dangerous in the arena of the investor.

The downside Sideliners are analytical and love running numbers hoping to reduce most risk by comparing return percentages. Yet, out of the paralysis of information, fear sets in, and they make minimal purchases to play it safe. The sideliner is a silent observer possessing discernment for weighing facts, yet witnesses other people’s investment success without taking action to enjoy investing personally.

The Gambler These people are confident thrill seekers who enjoy the casino, horse race, or scratch-and-win tickets, unlike the Sideliner. They confuse play gambling with risk tolerance, spend recklessly, consider that investment principles are for misers, and don’t seek the guidance of an advisor and consequently have a retirement portfolio that looks broke.

The downside The Gambler is comfortably numb and usually gets punished with frequent losses for taking above-average risks. They might buy an investment based on listening to the talking heads in the trading media, buy penny stocks, or low-priced failing company stocks — all based on uncredentialed hearsay. Because they think they might make some fast money, they believe they are investing but are not. Rarely does a Gambler stay invested for the long term.

The Hobbyists They buy things and investments based on their emotional value more than on investment value. As collectors, they buy for popularity status, notions of status, aesthetic gratification, and pleasure.

The downside Hobbyists, when excited, may jump to buy anything referred to them by word of mouth or a talk show host. They may own all the British Royal plaques on a wall or the top “500 must-see movies before you die”. Financial perspective gets lost because several investment funds may be bought by virtue of historic popularity instead of the potential for future gains. Because collections have been known to go up in value, they think they are investing. They do not understand the old Latin proverb “Non Quantum Sed Quale”, meaning it is not the quantity but the quality that counts.

The True Investor Utilizing an advisor’s wisdom, they buy suitable investments. Unlike Sideliners, they act. Unlike Gamblers, they minimise risk. Unlike Hobbyists, they buy based on investment value.

Investors are defined by their knowledgeable expectation for financial gain employing a principled process to minimise financial risk. Many also make it their practice to utilise professional managers and advisors when investing.

Actual investors act with a vision to achieve excellent returns on their investments while exposing themselves to mitigate the risk that suits their investor profile while enjoying the actions that lead to real financial success. It all comes down to how you think and whether you’re considering investment action.

Consider what is involved before naming or agreeing to act as an executor.

• An executor carries out the instructions in your will. Co-executors can share the task.

• Jurisdictional laws define what the executor must do, whether they are a friend, relative, professional, or a trust company—however, the will can specify even more extensive powers.

• The executor may have to deal with some or all of the following at an emotional time: a funeral home, beneficiaries, past or ongoing taxes, insurance and investment companies, government and business pension departments, real estate agents, lawyers, accountants, appraisers, stock brokers, and business partners.

• They may also be empowered to convert the estate to cash or divide assets equally among beneficiaries. They can also make payments to the parent/guardian of a beneficiary in most cases.

• The executor (especially if inexperienced in legal or financial matters) should know how complex the estate is before agreeing to the task. If necessary, appoint a co-executor who is a legal and accounting professional.

• Have a clear and objective idea of what will be involved before asking someone to be your executor and agreeing to act as one.

Discuss the parameters of an executor with your lawyer, before enabling one, or taking on the responsibility if given or offered to you.

By diversifying among carefully selected, different asset classes, you reduce the risk of being over-exposed to any particular asset class.

For example, an investor may hold assets such as bonds, GICs, balanced funds, equity funds, foreign equities, etc. The adage of “not putting all your eggs in one basket” applies to a diversified portfolio of assets. Having 10 different equity funds in a portfolio does not mean that an investor’s portfolio is diversified.

By diversifying among carefully selected, different asset classes, you reduce the risk of being over-exposed to any particular asset class.

By diversifying among carefully selected, different asset classes, you reduce the risk of being over-exposed to any particular asset class.