As parents, we need to consider the effect that education will have on the future income and lifestyle of our children. When Steve Jobs of Apple knew he had a short time to live, he became assertively interested and vowed that he would do everything in his power to ensure that his son received a good education.

As the Internet brings many changes quickly, we are seeing many manufacturers moving plants overseas. Stephen Covey, the best-selling author of The 7 Habits of Highly Effective People, predicted a need for technological education several years ago, echoing what we see everywhere: manufacturing increasingly calls for brain work rather than metal-bashing that empower the industrial age — further making a point:

The winds of education reform are beginning to stir once again. Our collective conscience is being nudged. And there’s a good reason. The world has moved into one of the most profound eras of change in human history. Our children, for the most part, are just not prepared for the new reality. The gap is widening. And we know it.

Parents see the chaos, the economic uncertainty, the stress and the complexity in the world, and know deep down that the traditional three “R’s” — reading, writing, and arithmetic — are necessary, but not enough.

Today robotics and artificial intelligence call for another education revolution. This time, however, simply cramming more schooling in at the start is not enough. People must also be able to acquire new skills throughout their careers.

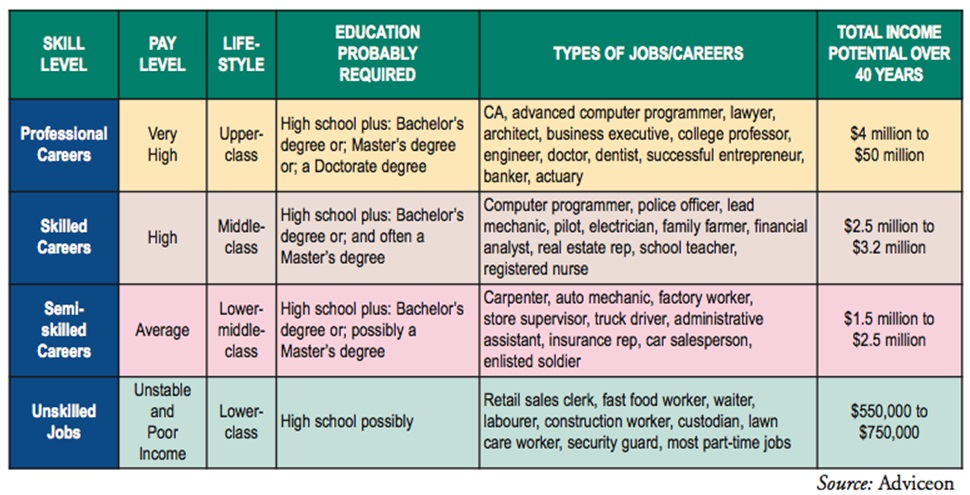

The following grid estimates the effect of educational decision-making on a child’s education. Income and future lifestyle can be severely affected by poor choices. When a child has the capacity and talent for a higher level of educational goal-setting and achievement, this needs to be developed appropriately.

What ways can we plan for our Child’s education? Consider using both the traditional Registered Educational Savings Plan (RESP) and the Tax-Free Savings Account (TFSA) as an educational savings vehicle. A TFSA offers parents another tax-efficient method to provide for education planning.

Using the TFSA for Educational Planning

Canadian residents age 18 or older can contribute up to a TFSA.

TFSA Contribution Limits

- 2009 to 2012: $5,000

- 2013 and 2014: $5,500

- 2015: $10,000

- 2016 to 2018: $5,500

- 2019 to 2022: $6,000

- 2023: $6,500

- 2024: $7,000

Contributions are not deductible from your taxable income. You can add any unused contributions of your annual limit, cumulative back to 2009.

Using the RESP for Educational Planning

- You can save for a child’s education using the RESP. The Government of Canada will also help you save money through the Canada Education Savings Grant (CESG).

- Your advisor can help you understand what RESP options is available to you in your province.

There are many compelling reasons to combine your investments in a tax-advantaged life insurance policy. Tax advisors have been pointing their wealthier clients to these unique policies for years. Let’s examine some of the tax benefits, investment options, overall features, and for whom they are best suited. Depending on the insurer, there can be many possible options, but all enjoy some of the following essential elements.

There are many compelling reasons to combine your investments in a tax-advantaged life insurance policy. Tax advisors have been pointing their wealthier clients to these unique policies for years. Let’s examine some of the tax benefits, investment options, overall features, and for whom they are best suited. Depending on the insurer, there can be many possible options, but all enjoy some of the following essential elements.

You can designate the number of years it will survive, within permissible, legal limits. The trust becomes effective at the time the will is probated. The assets undergo the probate process and are therefore, exposed to creditors’ claims. Note: If your intent is to avoid probate, a living trust would be a more suitable alternative especially adapting the use of life insurance. However the potentially lower marginal tax rates allowed with the testamentary trust, needs to be weighed against potentially higher future income tax payable. When using a testamentary trust (versus an inter vivos trust) make sure your beneficiaries are properly specified to work according to your trust directives. A qualified tax advisor should assist you as you make these decisions.

You can designate the number of years it will survive, within permissible, legal limits. The trust becomes effective at the time the will is probated. The assets undergo the probate process and are therefore, exposed to creditors’ claims. Note: If your intent is to avoid probate, a living trust would be a more suitable alternative especially adapting the use of life insurance. However the potentially lower marginal tax rates allowed with the testamentary trust, needs to be weighed against potentially higher future income tax payable. When using a testamentary trust (versus an inter vivos trust) make sure your beneficiaries are properly specified to work according to your trust directives. A qualified tax advisor should assist you as you make these decisions.