Here are some tips to help you lighten the load of Elder-Care:

• Plan your caregiving carefully. Don’t be ashamed to ask for and get help from your siblings or others when caring for a family elder—let others share the load—tell them how they can help, and let them know you expect it! They can clean, cook, take them to the doctor, shopping, or church, and take them to their home for a little break/holiday, etc.

• Be honest about what you can truly handle. Be honest about your time when you are home and what you can realistically achieve. Don’t let your housework stay undone due to your over-commitment to the elder. That isn’t fair to you or your family.

• Assess government and public resources. Find out what services are free or available as paid-for services—learn what your community offers in senior care.

• Prioritize your to-dos. In this way, you’ll know what needs immediate attention, such as their physical comfort and safety. Determine if any problems, such as a lack of heat or air-conditioning, water leaks, or mould accumulation in the elder’s environment, needs attention. Delegate help to family members or friends concerning their skill set, career, or financial ability to help.

• Assign care tasks to the elder that they can do. List the jobs to define what they can and can’t do. Involve the elder as far as possible in the plan, if they can cook their meals and bathe themselves, and let them know this is henceforth expected of them.

• Outsource where needed. Discuss who you might hire with the elder, and where applicable, expect their input in the decision. Maybe you must bring in a house-cleaner weekly and hire a handyperson.

• Let the elder assist you financially. You may be putting them up in a space in your home, and they might use your resources, so it is not out of line to ask them to help pay your bills (perhaps via rent). The elder is now retired, so they ought to reach into their investment income (if they have wisely invested or have gained other assets) or pension income to share in the expenses and perhaps buy and prepare their food.

• Decide to make informed decisions. Don’t procrastinate to make the necessary changes and improvements because years of frustration may accrue as “things unattended only to get worse”.

• Meet with a lawyer and financial advisor. If the relative increasingly depends on you to help in their estate planning, employ a good lawyer they can trust; write an up-to-date living and testamentary will.

• Review to determine if there may be life insurance needs for the funeral and burial expenses ahead of time. If there is, consider buying a policy and have siblings or heirs split the premium.

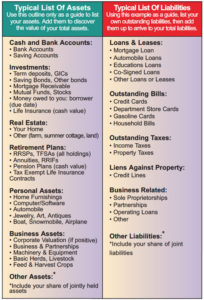

• Assess any tax and debt liabilities. Assess retirement savings, investment holdings, other assets and all liabilities to create a mini net worth snapshot to determine the potential net need for life insurance. Then select the amount necessary. Check if any cash values can make current cash income while maintaining an old policy the elder may own. Determine who will be the Power of Attorney (PA).

• Become an advocate. Don’t be afraid to take the elder’s side. Many are not used to today’s current culture and need kind understanding. So speak up for their rights and causes; never bully them or ignore their cries for help or justice as they face our healthcare system, unfair medicinal prescription fees, or rude gestures from others. Dialogue with physicians (and get second opinions) when necessary for their well-being.

• Maintain a happy attitude. If you keep your good humour and remain positive, you’ll lessen the stress factor. Caring for elders can tip your emotional scales, so laugh a little, even at yourself!

• Review and respect their historic life’s excellent and fun aspects with you. One day your elder won’t be around to show your appreciation and love for their positive role in your life. Tell respectful stories about their hero or heroine qualities. They probably did rescue you by overseeing your younger days while feeding and clothing you. Don’t put them down for failures—forgive them. They may have “been there” for you, so recall the best days of their life to realise they were needed, appreciated, and loved for who they are.

• Maybe write a book on their story. Why not review their life story in a journalised small book of their history—to leave a legacy to your family to show appreciation and take your mind off the stressful negatives? It may reveal redemptive qualities; to teach your younger generation by example—to impress the younger generation by the elder’s influence, such as perhaps: their character developed by war, or persistence during poverty, or a corrective life-change, their hard work that led to business success, or a healed relationship via forgiveness, or their involvement in charitable giving, or their volunteer work to help others, etc.

• Stay ahead of burnout. Get some rest and exercise weekly to protect your mental and physical health. Fulfil all your responsibilities, and maintain all your meaningful relationships. Be sure to get the R&R you need to stay graceful, strong and vigorous as your elder ages and becomes more dependent on you.

• Find unanimity in an elder-care support group. They can share their ideas and help you make decisions, help you not to feel alone, and help you face stresses and problems as they relate their wisdom obtained by experience. Getting ideas and compassion from other caregivers caring about you doesn’t hurt.

Caring for an older adult is not a job that comes with training or gets a lot of thanks—it is something you take on, usually out of love. It can be an unappreciated Herculean effort—but at least you’ll know you did your best at the end of the day. Your love is what counts.

Every so often, you can take a self-inventory and restate your primary purpose in caring for an elder. This will help you overcome the temptation to complain, throw in the towel, or send the elder to a rest home too early.

You may want to consider Longterm Care Insurance for yourself or your loved ones, which helps pay for services the family members may not be able to provide. Talk to your advisor about the life insurance policies available for these services.

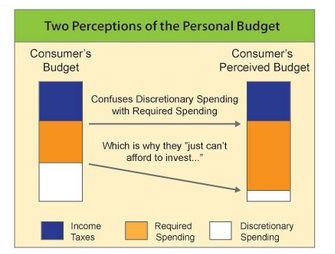

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?

Determine your perspective on investing. Always spending and never investing is a serious dilemma often based on a certain mindset that can easily change for the better. Do you view yourself as a consumer or an investor?

One way to cover the tax liability is to save for it. The problem arises if the owner dies too soon, or the money gets used for an emergency or a new opportunity, or if the savings goal is impossible for the company to achieve.

One way to cover the tax liability is to save for it. The problem arises if the owner dies too soon, or the money gets used for an emergency or a new opportunity, or if the savings goal is impossible for the company to achieve. Frequently review your capital gains tax liability. In some cases, the payment of relatively small life insurance premiums can entirely solve the estate’s future capital gains tax problems, and/or generate capital to replace the tax that will be payable on your RRSPs when both spouses die.

Frequently review your capital gains tax liability. In some cases, the payment of relatively small life insurance premiums can entirely solve the estate’s future capital gains tax problems, and/or generate capital to replace the tax that will be payable on your RRSPs when both spouses die.