The following advantages, make investing in mutual funds simple:

· Simplified investing You can select an industry or sector or country and/or currency within which a mutual fund trades securities. You do not have to to hand-pick each security. The mutual fund manager does this security selection process for you. You don’t have to be assessing which stock or bond may or may not be a winner. A fund manager is trained to weigh out all the market contingencies which can affect investor performance.

· Low-cost diversification A small monthly purchase plan can have you moving forward in your mutual fund investments in a day. Your money can buy a piece of many different investments held within one or more funds.

· Dollar-cost averaging Dollar-cost averaging allows you to buy more fund units when the unit values are down, less when they are high, giving you some benefit from downward volatility.

· Flexible access to your money You can sell your fund shares in one day. Your proceeds are available the next day if your money is needed in the short term.

· Portfolio balancing Choices include the full range of fund types, and strategies are available to use such as strategic balancing of your fund holdings.

· Automatically invest You can automatically invest more in mutual funds at any time or use dollar-cost-averaging.

· Professional management Mutual funds have active professional management watching over your investment.

The risk/reward concept states that the higher the risk of a particular investment, the higher the possible return. Although there is usually risk with any equity investment, assessing just how much risk your portfolio should carry is essential. Risk involves the potential for gain or loss of monies invested.

Many people take on more risk, hoping to achieve a higher return without regard to cyclic markets. If an investor expects higher returns based on the past, he must understand that markets can go through gain and loss periods.

In theory, many think that the higher the risk, the more you should receive for holding the investment. With cyclic markets, this is not necessarily true. Conversely, in theory, the lower the risk, the less you should receive. Unfortunately, the dilemma is this: a higher potential for above-average returns comes with a higher risk of below-average returns. Conversely, safer investments, such as cash and bond instruments, have a lower potential for high returns and a higher potential to not keep up with inflation.

While choosing investments for your portfolio, you need to be conscious of risk/return trade-offs and risk tolerance. Different types of securities have associated levels of risk. Every investor’s goal should be to find a balance that allows you to not experience undue anxiety in the markets and achieve your long-term financial goals at the same time.

Psychological fear can hold one back from investing. People behave according to their mindset. Some of the following thinking can keep one from not putting their money to work by buying equity investments such as equity investment funds. If you have said any of the following statements, you may be experiencing investor anxiety:

“I think the markets will pull back and lose some value.” I will wait and invest when this happens.” This viewpoint is based on the need to confirm a belief before acting, where the investor must minimize any evidence that contradicts their belief mantra. The media frequently offers terrible news if the market has a low day, and it is easy to hear only this information while filtering out other positive news. This process can paralyze an action plan to invest for years.

“I want to sell the investment if I see a profit.” People might sell an investment early once it rises in value for fear of future loss. Aside from considering taxation, once sold, an investment with either a gain or a loss ends any future potential of that investment rising in future value. To avoid this mindset, one should have a disciplined written plan for buying and selling assets that can be frequently referred to.

“The market is bound to correct and head down because it is at a peak.” Anchoring our point of view occurs when someone assigns a reference number, like a 52-week high or low, to compare the price of an investment stock, the unit value of a fund, or a stock exchange’s last peak value. Past price movements are poor predictors of future price performance. When you invest for the long-term for retirement, using past price patterns is comparable to driving your car while gazing in the rearview mirror as a reference.

Conclusion

The above emotional mindsets can ruin or avoid forming an otherwise excellent investment plan. They can help you develop a risk tolerance profile and investment plan. Please work with your investment advisor to help you understand how the mind can trick us into failure simply by not investing over the long term.

“Individuals who cannot master their emotions are ill-suited to profit from the investment process.” Benjamin Graham

A good financial advisor will not only assess your current fiscal resources. They will also outline a plan to achieve your goal for a sound financial future.

As time passes, so does your opportunity to build a solid financial future. Suppose you are to develop an investment portfolio and a significant net worth. Will you personally determine how to purchase stocks among the international markets, analyse investment funds, and sidestep economic pitfalls as you invest all by yourself? Will your financial stability be based on our government’s pension plan? Did you know that its maximum benefit covers only 25% of the average Canadian’s wage?

Why involve an advisor in your financial affairs?

The majority of Canadians seek specialised professional help. Their work is to guide you towards achieving financial independence. An advisor’s work is to help you systematically achieve your goals and make your life dreams come true.

• An advisor must analyse your current financial resources to define appropriate financial strategies that are best suited to your current and future personal priorities, retirement goals and risk tolerance.

• Calculating your current net worth and cash flow after taxes is also essential. With a net worth statement, a financial specialist can identify any opportunities or problems relating to capital gains, life insurance, disability, and critical illness insurance needs versus your present coverage, investment growth, income taxation, retirement income needs, employee benefits, and potential capital gains tax liabilities for your estate. Parents must also assess educational funding needs and plans for any dependent adult child and special health care such as Long Term Care (LTC) for parents.

• Establishing a written plan sets forth specific solution-oriented recommendations and will enable you to see how ordering your finances can benefit your overall lifestyle.

• To achieve your goals and objectives, acting on the plan’s recommendations will be necessary. Building a solid portfolio of investments tailored to meet your goals and risk tolerance is essential for your future financial independence.

• Appropriate life and disability insurance coverage will ensure your plan meets family income needs, business debt or buy-out payments, and any tax liabilities for your estate.

• Finally, an advisor will establish a periodic review to monitor and refine your plan to accommodate birth, marriage, illness, or retirement events.

Diversification is a strategy by which you create a portfolio that includes several investments. You make investments over more stocks of different companies or securities, such as bonds or mortgages, with the objective of reducing risk.

Because of their higher risk, equity funds have historically offered the most promising growth over the long term, as compared with other funds that focus on assets such as bonds and cash. In markets that are volatile, how can we reduce the overall equity volatility over the long haul without losing the potential for gains?

In a volatile market, if you shift the asset class out of equities into bonds and/or cash prior to resurgence in the overall market, you can lose by trying to automatically time the market. Why is this? Most stocks increase in value through a new bull market period which can begin quickly over several days. By being out of the equity market (in this case at the wrong time), you could lose the gains you might have achieved by being more heavily invested in equity funds.

Understand geographic diversification.

Global equity markets are more closely correlated than they were five or ten years ago, reacting to world events in a more similar fashion. Technology has connected our world to make it a smaller place, so what happens today in China’s market can impact economies everywhere. And more importantly, global diversification offers scant protection from market crashes when correlations become indistinguishable, such as during the financial crisis of 2008–2009.

However, it is still prudent to have portfolios that offer geographic diversity, rather than focusing exclusively on a single geographic equity market.

Estate Planning is a financial planning process that every responsible working person with dependents should accomplish, even if it is preparing a last will and testament and living will for health purposes.

Estateplanning can empower your heirs in the following ways:

Plan to reduce taxes in your estate When transferring your assets, including mutual funds, using a will, try to pass as much value as possible to your heirs. If you hold equity mutual funds that buy and hold stocks, they may have accrued capital gains. There will be a deemed disposition of all your property at fair market value at the time of your death. For some this could mean a capital gains tax liability.

By knowing your estate tax liability List each separate asset you own, the purchase price and date, as well as its current value. Include your non-registered investments in stocks, bonds, and mutual funds. Have your accountant assess what the tax liability will be.

Your spouse and deferred taxes Property willed to your spouse can be rolled over tax-free on your death. Your spouse will actually inherit the assets at the unchanged adjusted cost base (cost amount) of the property. The taxation of the asset will then occur when your spouse disposes of the property or at the death of the spouse. This tax deferral is beneficial especially if you have large holdings in equity mutual funds invested for value as in large cap or blue chip stocks. Alternatively, you can choose to transfer any asset to your spouse at fair market value on death and recognize the accrued gain or loss.

RRSPs and your children Under the rules proposed in the 1999 Federal Budget, RRSPs can be transferred tax-deferred to your dependent children or grandchildren, even if a spouse survives you. Before the 1999 Federal Budget, a transfer of RRSP funds to dependent children or grandchildren would be taxable if there was a surviving spouse.

Income splitting using a testamentary trust By establishing a testamentary trust in your will, you will be able to maintain control during your lifetime over the use of your assets such as a mutual fund investment portfolio. The trust can provide guidelines for the treatment of these assets after your death. The trust document can specify the split of income among heirs. Carefully planned income splitting may allow for significant tax savings.

Assess your tax liabilities with an estate lawyer and/or accountant and make estate plans to determine how to pay them. Consider the use of life insurance where the capital gains tax liabilities are substantial.

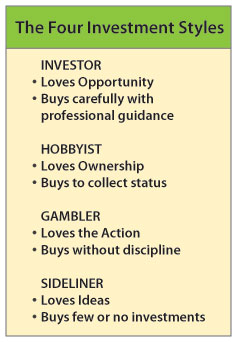

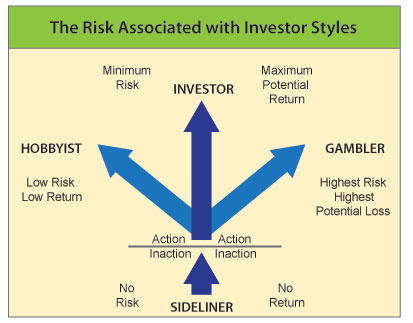

There are four basic types of people, each with differing mindsets when they approach investing; the Sideliner, the Gambler, the Hobbyist, and the True Investor. If you want to be a serious and successful investor, you must mindfully recognise the erroneous attitudes of the Sideliner, the Gambler, and the Hobbyist.

The Sideliner Sideliners are fearless in taking action as long as they are in the audience and won’t ever get bruised. They shout, stand, and clap, loving the action of a bystander. Sideliners love the excitement of stock market news and the investor’s game. They often look at how the indices, a stock, or a fund performed. Observation alone never gets you in the game of investing. Sideliners may feel it is dangerous in the arena of the investor.

The downside Sideliners are analytical and love running numbers hoping to reduce most risk by comparing return percentages. Yet, out of the paralysis of information, fear sets in, and they make minimal purchases to play it safe. The sideliner is a silent observer possessing discernment for weighing facts, yet witnesses other people’s investment success without taking action to enjoy investing personally.

The Gambler These people are confident thrill seekers who enjoy the casino, horse race, or scratch-and-win tickets, unlike the Sideliner. They confuse play gambling with risk tolerance, spend recklessly, consider that investment principles are for misers, and don’t seek the guidance of an advisor and consequently have a retirement portfolio that looks broke.

The downside The Gambler is comfortably numb and usually gets punished with frequent losses for taking above-average risks. They might buy an investment based on listening to the talking heads in the trading media, buy penny stocks, or low-priced failing company stocks — all based on uncredentialed hearsay. Because they think they might make some fast money, they believe they are investing but are not. Rarely does a Gambler stay invested for the long term.

The Hobbyists They buy things and investments based on their emotional value more than on investment value. As collectors, they buy for popularity status, notions of status, aesthetic gratification, and pleasure.

The downside Hobbyists, when excited, may jump to buy anything referred to them by word of mouth or a talk show host. They may own all the British Royal plaques on a wall or the top “500 must-see movies before you die”. Financial perspective gets lost because several investment funds may be bought by virtue of historic popularity instead of the potential for future gains. Because collections have been known to go up in value, they think they are investing. They do not understand the old Latin proverb “Non Quantum Sed Quale”, meaning it is not the quantity but the quality that counts.

The True Investor Utilizing an advisor’s wisdom, they buy suitable investments. Unlike Sideliners, they act. Unlike Gamblers, they minimise risk. Unlike Hobbyists, they buy based on investment value.

Investors are defined by their knowledgeable expectation for financial gain employing a principled process to minimise financial risk. Many also make it their practice to utilise professional managers and advisors when investing.

Actual investors act with a vision to achieve excellent returns on their investments while exposing themselves to mitigate the risk that suits their investor profile while enjoying the actions that lead to real financial success. It all comes down to how you think and whether you’re considering investment action.

Consider what is involved before naming or agreeing to act as an executor.

• An executor carries out the instructions in your will. Co-executors can share the task.

• Jurisdictional laws define what the executor must do, whether they are a friend, relative, professional, or a trust company—however, the will can specify even more extensive powers.

• The executor may have to deal with some or all of the following at an emotional time: a funeral home, beneficiaries, past or ongoing taxes, insurance and investment companies, government and business pension departments, real estate agents, lawyers, accountants, appraisers, stock brokers, and business partners.

• They may also be empowered to convert the estate to cash or divide assets equally among beneficiaries. They can also make payments to the parent/guardian of a beneficiary in most cases.

• The executor (especially if inexperienced in legal or financial matters) should know how complex the estate is before agreeing to the task. If necessary, appoint a co-executor who is a legal and accounting professional.

• Have a clear and objective idea of what will be involved before asking someone to be your executor and agreeing to act as one.

Discuss the parameters of an executor with your lawyer, before enabling one, or taking on the responsibility if given or offered to you.

Too much debt can threaten your future and destroy your peace of mind. Here are five warning signs to watch for:

You are spending more than 20% of your after-tax earnings on debt. Total up all you owe, excluding your mortgage, e.g. student loans, car payments, and credit card bills. Now total up how much of your after-tax income is dedicated to servicing this debt.

You are paying for daily essentials with credit instead of cash. Consequently, you are close to the credit limits on your cards. Credit cards charge notoriously high interest rates, which is exasperated by compounding when credit cards are not paid off monthly. This can also increase your actual gross cost of goods purchased.

You are deferring important expenditures. You may need maintenance work (on your car, your home, and your teeth) as you struggle to get by.

You seem to spend your paycheque the day you get it. This may be a sign that you’re also over spending, an activity that leads to debt.

You are not differentiating between ‘good’ versus ‘bad’ debt. Good debt is money borrowed for productive purposes to help generate wealth over time (such as an education, build a small business, or purchase real estate). Fancy cars, expensive vacations, restaurant meals, and over-indulgent gift giving may indicate a lifestyle that for many do not justify the average household’s paycheque.

If you are in serious debt, consult a debt counselor who will arrange a repayment schedule with your creditors.

Consumers are shifting unsecured high-interest credit card balances and debts such as car loan balances to a low-interest Home Equity Line of Credit (HELOC). This transference happens on a larger scale when people consolidate their debts while backing them with their home value. Once your home secures this debt, it is no longer unsecured debt in your portfolio.1

You may indeed be able to save a sizeable chunk of interest by transferring debt from a high-interest credit card to a low-interest HELOC. For many, this works well insofar as they have an intelligent debt repayment plan in place.

When developing a financial strategy, assess all of your credit cards and other loans, including a Home Equity Line of Credit (HELOC). Total your combined debt while you weigh this against all of your retirement and your non-retirement assets.

A safety precaution always estimates your decisions about how they will impact your net worth statement when subtracting liabilities from assets. Adding in your HELOC debt with your portfolio of obligations gives you proportional insight into your actual net worth. Add your HELOC level of debt alongside your unsecured credit cards. Compare interest rates, fees, and other features and the time it will take to pay these loans all off (some calculators do a great job comparing this).

That said, be cautious using HELOC debt as quick loans for vacations, 2nd residences, extensive renovations versus selling and repurchasing a new home, vehicles, businesses, or investments. HELOC credit cards offered with most lines of credit will also reduce your home equity value.2

This growing shift of unsecured credit card debt to HELOC debt enticed by lower interest rates (related to your mortgage) helps the lenders’ balance sheets because this debt, once transferred, becomes secured collateral against real estate assets then owned at a higher proportion by the bank. Taken to the limit, if the real estate market prices drop, your debt may surpass your home value — this happened in the 2007-8 mortgage debt crisis. Think seriously about reducing your debt portfolio, especially if you hold a lot of HELOC debt.

Many people are inadvertently reducing their home equity in the process of securing previously unsecured credit card debt while hinging it to and reducing their home value. When people sell their homes, they are often surprised that their home equity is considerably reduced after paying their mortgage. Why is this? You must pay all associated HELOC debt during the sale.

Source: Bank of Canada

1 Most credit cards are unsecured by any asset that you own. However, if you accept a credit card linked to your home which offers low interest, this may be secured against your home value. Many consumers are unaware of how this works.

2 If bankruptcy occurs, your home equity generally is safe unless it is secured against HELOC debt. Unsecured credit cards are often simply not necessary to repay should one seek bankruptcy protection. Always read your small print in all contracts. Don’t rely on sales discussions over the phone or in-person until you read the small print. It is only beneficial to a bank or financial institution to shift your debt from unsecured credit card debt to secured debt if bankruptcy ever does occur.

Too much debt can threaten your future and destroy your peace of mind. Here are five warning signs to watch for:

Too much debt can threaten your future and destroy your peace of mind. Here are five warning signs to watch for: