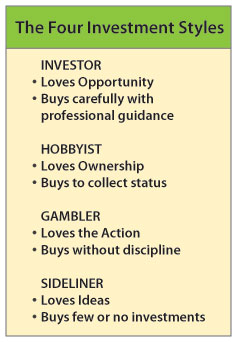

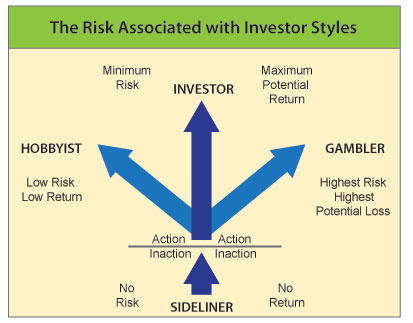

There are four basic types of people, each with differing mindsets when they approach investing; the Sideliner, the Gambler, the Hobbyist, and the True Investor. If you want to be a serious and successful investor, you must mindfully recognise the erroneous attitudes of the Sideliner, the Gambler, and the Hobbyist.

The Sideliner Sideliners are fearless in taking action as long as they are in the audience and won’t ever get bruised. They shout, stand, and clap, loving the action of a bystander. Sideliners love the excitement of stock market news and the investor’s game. They often look at how the indices, a stock, or a fund performed. Observation alone never gets you in the game of investing. Sideliners may feel it is dangerous in the arena of the investor.

The downside Sideliners are analytical and love running numbers hoping to reduce most risk by comparing return percentages. Yet, out of the paralysis of information, fear sets in, and they make minimal purchases to play it safe. The sideliner is a silent observer possessing discernment for weighing facts, yet witnesses other people’s investment success without taking action to enjoy investing personally.

The Gambler These people are confident thrill seekers who enjoy the casino, horse race, or scratch-and-win tickets, unlike the Sideliner. They confuse play gambling with risk tolerance, spend recklessly, consider that investment principles are for misers, and don’t seek the guidance of an advisor and consequently have a retirement portfolio that looks broke.

The downside The Gambler is comfortably numb and usually gets punished with frequent losses for taking above-average risks. They might buy an investment based on listening to the talking heads in the trading media, buy penny stocks, or low-priced failing company stocks — all based on uncredentialed hearsay. Because they think they might make some fast money, they believe they are investing but are not. Rarely does a Gambler stay invested for the long term.

The Hobbyists They buy things and investments based on their emotional value more than on investment value. As collectors, they buy for popularity status, notions of status, aesthetic gratification, and pleasure.

The downside Hobbyists, when excited, may jump to buy anything referred to them by word of mouth or a talk show host. They may own all the British Royal plaques on a wall or the top “500 must-see movies before you die”. Financial perspective gets lost because several investment funds may be bought by virtue of historic popularity instead of the potential for future gains. Because collections have been known to go up in value, they think they are investing. They do not understand the old Latin proverb “Non Quantum Sed Quale”, meaning it is not the quantity but the quality that counts.

The True Investor Utilizing an advisor’s wisdom, they buy suitable investments. Unlike Sideliners, they act. Unlike Gamblers, they minimise risk. Unlike Hobbyists, they buy based on investment value.

Investors are defined by their knowledgeable expectation for financial gain employing a principled process to minimise financial risk. Many also make it their practice to utilise professional managers and advisors when investing.

Actual investors act with a vision to achieve excellent returns on their investments while exposing themselves to mitigate the risk that suits their investor profile while enjoying the actions that lead to real financial success. It all comes down to how you think and whether you’re considering investment action.

You can designate the number of years it will survive, within permissible, legal limits. The trust becomes effective at the time the will is probated. The assets undergo the probate process and are therefore, exposed to creditors’ claims. Note: If your intent is to avoid probate, a living trust would be a more suitable alternative especially adapting the use of life insurance. However the potentially lower marginal tax rates allowed with the testamentary trust, needs to be weighed against potentially higher future income tax payable. When using a testamentary trust (versus an inter vivos trust) make sure your beneficiaries are properly specified to work according to your trust directives. A qualified tax advisor should assist you as you make these decisions.

You can designate the number of years it will survive, within permissible, legal limits. The trust becomes effective at the time the will is probated. The assets undergo the probate process and are therefore, exposed to creditors’ claims. Note: If your intent is to avoid probate, a living trust would be a more suitable alternative especially adapting the use of life insurance. However the potentially lower marginal tax rates allowed with the testamentary trust, needs to be weighed against potentially higher future income tax payable. When using a testamentary trust (versus an inter vivos trust) make sure your beneficiaries are properly specified to work according to your trust directives. A qualified tax advisor should assist you as you make these decisions.

Too much debt can threaten your future and destroy your peace of mind. Here are five warning signs to watch for:

Too much debt can threaten your future and destroy your peace of mind. Here are five warning signs to watch for:

Many who own family businesses, will move into retirement over the next two decades. A delicate process referred to as “succession” or “business continuity” planning can lead to relinquishing leadership roles while transferring their businesses to the next generation.

Many who own family businesses, will move into retirement over the next two decades. A delicate process referred to as “succession” or “business continuity” planning can lead to relinquishing leadership roles while transferring their businesses to the next generation.